When you hear the words "retirement destination," places in Arizona and Florida probably spring to mind. But broaden your horizons, and you can find plenty of other great options all across the country.

The following 15 spots may not be popular with retirees now-but contrarian living comes with benefits. Some of these places may offer tax breaks or other perks to try and lure in more older residents. Plus, the existing younger crowds might help keep you young and active.

Check out our list of surprising places for retirement that you probably haven't considered, and see if any hold appeal for your own new home:

Chick-fil-A is among the most successful fast-food chains in the US, and it's also one of the cheapest to open.

The company grew by $700 million to achieve $5.8 billion in sales in 2014, making it larger than every pizza brand in the country, according to QSR magazine.

Chick-fil-A is now the eighth-largest fast-food chain in the US by sales, and it generates more revenue per restaurant than any other chain nationally, according to QSR.

Despite its success, Chick-fil-A charges franchisees only $10,000 to open a new restaurant, and it doesn't require candidates meet a threshold for net worth or liquid assets, the company told Business Insider.

That's cheaper than every major fast-food chain in the US.

McDonald's, for example, requires potential franchisees to pay between $955,708 and $2.3 million in startup costs - including a $45,000 franchise fee - as well as have liquid assets of at least $750,000.

Taco Bell's startup costs average $1.2 million to $2.5 million and the company requires a minimum net worth of $1.5 million and liquid assets of at least $750,000.

Chick-fil-A, on the other hand, pays for all startup costs - including real estate, restaurant construction, and equipment.

In turn, the company leases everything to its franchisees for an ongoing fee equal to 15% of sales plus 50% of pretax profit remaining, Chick-fil-A spokeswoman Amanda Hannah told Business Insider.

"The barrier to entry for being a franchisee is never going to be money," Hannah said. "We seek to find the very best business partners who find great joy in making other people's days. They do so with a combination of great business acumen, an entrepreneurial spirit, and a passion for serving others."

So what's the catch?

While Chick-fil-A's startup costs are low, the ongoing fees are higher than those charged by many of its rivals.

McDonald's, for example, charges an ongoing monthly service fee equal to 4% of gross sales and an additional fee for rent, which is also a percentage of sales. McDonald's franchisees have historically paid about 8.5% of sales in rent costs, though some pay as much as 12%, according to a 2013 Bloomberg report.

Chick-fil-A also prohibits most of its franchisees from opening multiple units, which can limit franchisees' potential profits.

This limitation is meant to enable Chick-fil-A's franchisees to be intimately involved in the day-to-day operations of their restaurants.

"Chick-fil-A operators must be as comfortable rolling up their sleeves in the kitchen as they are shaking hands in the dining room," Hannah said.

The company also puts a big emphasis on community service and encourages franchisees to be actively involved in the communities where they live and work.

"Oftentimes, several operators in a market will combine resources to market events through advertising and promotion," Hannah said. "Our daddy-daughter date nights are an example of this."

The application process

Chick-fil-A gets more than 20,000 inquiries from franchisee candidates every year. From those candidates, Chick-fil-A selects between 75 to 80 new franchisees annually, Hannah said.

Chick-fil-A will then contact the candidates for interviews. The company may also interview candidates' friends, family members, and business partners.

Once they are selected and hired, franchisees have to undergo a multi-week training program before they can open and operate their own restaurant.

Car salespeople aren't necessarily evil, but they're the only people who can prevent you from getting the best price for your next car. It's a good idea to keep these four car dealer traps in mind the next time you decide to go car shopping. Doing so might save you the gut-wrenching regret of being screwed over and forced to overpay for your new vehicle.

When the salesperson starts talking about monthly payments, watch out.

Clever salespeople want you to focus only on low monthly payments because it gives them room to inflate other variables, such as the loan interest and length. This increases the dealer's profit - while you spend thousands more on the car overall.

Some dealers pull out what's called a four-square chart, which is confusing as hell. A former car salesman unveiled on The Consumerist how that shell game is played: You're put on the defensive and worn down with tricky math, while the salesperson appears to knock down prices.

Counter Strategy: Don't even discuss monthly payments. Tell the salesperson you can talk financing later, but first want to know their best price.

Pay for the car in cash or get your own financing if you can, but don't reveal how you're going to pay until after you've negotiated down the total car price. (Dealers may be less likely to negotiate if they know they can't profit from your financing.)

If you do need to discuss dealer financing, do that after you've negotiated the car price. From there you can focus on the annual percentage rate (APR) rather than payments.

Dealer Trick #2: Telling You Your Credit Sucks

If you don't know your credit score, all dealerships have to do to rip you off is say you don't qualify for a better rate. Perhaps a bank would offer a 5% loan; the dealer might say 7% is the lowest for your credit score.

Counter Strategy: Pull your credit report for free and know your credit score before setting foot in a dealership. Again, shop around for financing and get it on your own if you can. Whatever your credit score, at least you'll know if the dealer's trying to pull a fast one on you.

Salespeople can disarm you with humor and appear to be on your side in your battle against a faceless manager in the back room. You might even get a great trade-in offer or discount on the total price.

Inevitably, lowball offers and inflated trade-in values are squashed by the manager later. Edmund.com's Confessions of a Car Salesman series reveals how numbers previously agreed upon can somehow be "lost" or "forgotten" by the dealership.

Counter Strategy: Not all car salespeople are scumbags, but remember, they're doing their jobs and are not your friends. Don't fall for the good guy/bad guy game, and walk if they don't honor what you agreed upon. Better yet - get a copy of the numbers in writing from the dealership.

Dealer Trick #4: Pushing Add-Ons and Fees

Finally, be on the lookout for extras added to your purchase or financing. Dealers can increase your car payment price by "packing" extras like an extended warranty, perhaps saying it's "only $40 more" a month. That $40 extra will cost you $2,400 over a 60-month loan.

Counter Strategy: Know which add-ons are truly unnecessary and check the financing and sell sheets carefully. Things you shouldn't be charged for include a hidden loan acquisition fee and other fees, such as "customer service" or doc preparation fees.

You only need to do two things to come out on top: research car prices and comparison-shop multiple dealerships. One recent car survey found that knowing the dealer's invoice prices and visiting two dealerships saved car buyers an average of $800. TrueCar, Kelley Blue Book and Edmunds.com can all help you find invoice prices and what your trade-in is worth.

My favorite method is simply this one published on GetRichSlowly.com: email all of the dealers near you and say, "Hi, my name is so and so. I plan to buy such and such a car today at 5pm. I'm going to buy it from the dealer who gives me the best price. What is your best price?" Bam. Straight to the chase.

People move for many different reasons. For instance, some get new jobs, others retire, and some just want to be closer to their families.

While many people in the US move within the same state - the Census Bureau estimated in 2011 that 40% of moves are within 50 miles - there are patterns for those who did make interstate moves, according to Atlas Van Lines, a national moving company.

Atlas looked at 77,705 interstate moves and found that 18 states had more people moving out than in, whereas 12 had the reverse happen. We rounded up the 18 that had outflows for 2015. Most are in the upper-Midwest, which Atlas said has been on an outbound trend for a while.

"The Midwestern states experienced a major shift to outbound moves, with Wisconsin, Iowa and South Dakota going from balanced to outbound in 2015," said the report. "Similar to 2013 and 2014, North Dakota was the only state in the region to register as inbound."

See the states that topped the list, in order from lowest to higher percentage outbound migration:

National banks are still struggling to shed their collective image as fee-heavy, profit-hungry machines. Despite this reputation, however, national brick-and-mortar banks offer numerous products and services that consumers are still happy to use.

Ubiquitous branches and ATMs, interest-bearing accounts and state-of-the-art technology make the larger, commercial bank the right fit for consumers who need their bank to be everywhere - and who need digital banking services or a wide range of insurance and loan options that many smaller, community financial institutions don't offer.

With so many product and service factors to consider, choosing the right bank with the right blend of amenities to fulfill your needs can be a challenge. Moreover, you want to make sure you're choosing a bank that offers competitive interest rates.

Personal finance website GOBankingRates.com conducted its annual Best Banks study to help you narrow your search. The study assessed the top 90 financial institutions based on asset size according to the FDIC. Check out the top 10 banks to see what they have to offer.

Best Bank: Wells Fargo

Although it doesn't have the highest number of ATMs, Wells Fargo does have the most U.S. branches of any national brick-and-mortar bank on this list - 6,200. It also has other advantages that make it the best bank of 2016. Wells Fargo's array of deposit products, loan and investment service options, and smartphone banking capabilities are hard to match, and it has a BauerFinancial rating of four.

Bank of America

Although its $12 checking account fee is one of the highest on this top 10 list, Bank of America offers a high level of convenience. With more than 16,100 ATMs scattered across the country, customers have the accessibility they need to deposit or withdraw on the go.

Chase

Like Bank of America, Chase's $12 checking account fee is high compared with other banks on this list, but the bank offers a broad range of products that result in convenient banking options. Accessibility through its 5,300 branches and 15,500 ATMs is a major feature for Chase because, although its savings rate of 0.01 percent APY is similar to many banks on this list, its 0.02 percent APY CD rate is one of the lowest on this list.

Citibank

Citibank offers customers a thorough product list, including several credit card choices, from secured and student cards, to rewards, business and travel credit cards. It also offers several investment options for wealth building. It has one of the highest checking fees on this list ($12) but also one of the highest CD rates (0.15 percent APY).

First Midwest Bank

First Midwest Bank is the other financial institution on this list with no checking account fee. Although its branch locations are limited to Illinois, Indiana and Iowa, the bank offers access to more than 50,000 ATMs nationwide through its Allpoint network.

First Niagara Bank

First Niagara Bank offers the highest 12-month CD rate of the Best Banks of 2016: 0.50 percent APY on a $500 minimum opening balance. It also offers the highest savings account rate of any bank on this list at 0.10 percent APY. The bank has nearly 400 branches across Connecticut, Massachusetts, New York and Pennsylvania.

Great Western Bank

Great Western Bank is one of only two financial institutions in this top 10 with no checking fee. It also boasts a 0.15 percent APY CD; a full range of deposit account products as well as loan, investment and insurance services; and a BauerFinancial rating of five. However, its 158 branches are located in the West and Midwest only.

HSBC Bank

If a basic, no-frills checking account is what you want, HSBC is a top choice. Its Basic Banking account carries a fee of just $3. Consumers looking for more features might want to opt for the bank's Choice, Advance or Premier Checking products, which offer additional credit card and relationship savings account options.

PNC Bank

PNC Bank offers a full range of banking and finance products and services, including brokerage accounts, stocks and bonds, education accounts and insurance. It also has the second-highest savings account rate on this list - 0.05 percent APY - if you have a PNC checking account. The checking account has a $7 monthly fee.

U.S. Bank

U.S. Bank has a higher-than-average 12-month CD rate (0.10 percent APY) and a slightly lower checking fee ($6.95) than many of its competitors. It also offers a range of deposit services, credit cards and mortgage and auto loans.

All the top 10 banks of 2016 received a BauerFinancial rating of at least 4 out of 5. Although their deposit account rates are about average, or in some cases lower, compared with what some smaller financial institutions and online-only banks can offer, these national brick-and-mortar banks offer a significant range of banking products, digital money management capabilities, widespread branch and ATM access, and loans and investing services that smaller and online institutions cannot.

Methodology: Rankings were based on criteria such as deposit account interest rates for checking, savings and 12-month certificate of deposit accounts; diversity of products offered, such as auto loans, mortgages, credit cards and investment services; the banks' accessibility in terms of branch and ATM locations; and their BauerFinancial star ratings.

Millennials have had a rough road when it comes to money. Not only did they come of age during the Great Recession, which made jobs scarce and benefits even scarcer, but many saw their parents lose big time in the stock or real estate markets, which scared them off of making their own investments. Still, there's no more time for excuses, because millennials are all grown up and taking on increasing amounts of responsibility. From mortgages and parenthood to caring for aging parents, millennials are facing big financial milestones, whether they're ready or not.

According to Bank of America's Year-End Millennial Snapshot, which analyzed 2015 data from over 3,500 millennials, this young cohort of 20- and early 30-somethings continues to struggle financially: a tough job market, hesitancy to invest and student loans are just a few of the challenges in their way to prosperity. Still, the data suggest they are firmly committed to achieving financial independence one day. About half of millennials said the Great Recession changed the way they think about saving, investing and spending, with 40 percent saying they are more reluctant to invest in the stock market and 36 percent saying they are more hesitant to buy a house.

Yet over 80 percent of millennials are optimistic that they will be able to save and invest more in the future. "There is still a sense of optimism with the millennials. Although they're more hesitant, it's not stopping them. They feel good about the future," says John Jordan, client experience and programs executive for preferred and small business banking at Bank of America.

Many are also getting some big financial assists from their parents, and 46 percent of millennial-supporting parents say they don't plan to stop anytime soon.

A survey by the investment app Acorns of 1,020 millennials found that almost half of those surveyed said they were "treading water" financially or worse and would be in big trouble if they missed a paycheck. Most millennials (85 percent) said they haven't yet invested any money in the stock market, largely because they don't feel comfortable with it. While respondents said they wanted to save more, they found it difficult to do so given the pressures of living expenses and student loans.

"So many millennials are working on a contract basis or as freelancers; they don't have full-time benefits," says Jennifer Barrett, vice president of editorial and founding editor of Grow, a digital magazine published by Acorns and aimed at millennials. "They have to be more proactive ... [and] engage with finances much earlier than with earlier generations. Millennials are on their own in a lot of ways," she says.

That's why forming good money habits is a key part of creating financial stability for the millennial generation, Barrett adds. "We recommend that people get in the habit of investing early on," she says.

That's a message echoed by other millennial financial experts. "The biggest money mistake most people make - and I know I certainly did - is simply waiting too long to care," says David Weliver, 34, founder of the millennial finance website Money Under 30. When you're juggling your career, love life and other big issues, it's hard to also find time for your finances.

After college, young people tend to get bombarded with credit card offers, Barrett says, but they're usually better off skipping them. If you take on credit card debt, especially on top of student loan debt, then it's easy to get stuck in a trap of constantly feeling like you're falling behind. "Some millennials are embarrassed by [their debt]; it weighs pretty heavily on them," she adds.

2. Increase your savings whenever you get a raise.

Anytime you experience a windfall - perhaps you earned a bonus or got a raise - Barrett suggests putting it directly into your retirement savings. "If you can increase your contribution right away before you have time to even register that you have a raise, that's what really makes the difference," she says.

3. Get comfortable with investing.

Because so many millennials are scared of investing in the stock market (and understandably, since they came of age during the Great Recession), Barrett says it's particularly important to dive in early so long-term savings can outpace inflation. At the same time, though, she adds that it's important to have an emergency fund stashed in a safe spot, like a bank account, so you can cover unexpected expenses without reaching for a credit card.

4. "Stop the bleeding."

That graphic expression is how Weliver describes the need to prioritize. "Make sure you're not going into more debt," he says, adding that you should look for ways to downsize your lifestyle or earn more money (or both). Once you find a way to end the month positive at least a couple hundred dollars, then you can start making choices about saving, investing and paying off debt.

5. Pay off student debt.

Student loans are the albatross that hounds so many millennials; Weliver still remembers the day he made his final payment. Along with the day he realized he had enough in savings to live on for a year if necessary, it was a momentous occasion, and one that reinforced his choice to be more conscious about his spending and money management.

6. Imagine your future.

Considering where you want to be down the road can help you make the right choices today, Weliver adds. While taking out insurance or funding retirement aren't the most exciting investments now, they could save you from financial challenges in the future.

7. Embrace your earning power.

If you're working entry-level jobs or getting by on sporadic freelance work, then it's hard to feel in control of your finances, warns Stefanie O'Connell, 29, author of "The Broke and Beautiful Life," a money guide for millennials, and contributor to the U.S. News Frugal Shopper blog. "Even if you reduce your monthly expenses to zero, you're only saving as much as you were once spending ... I tripled my income in 2015 and it's been absolutely life changing," she says.

O'Connell adds that given today's tough job market, millennials have to show initiative and aggressively pursue higher-earning opportunities. "Take the initiative to show how you contribute to the bottom line. It's hard to argue against a raise when you have the numbers and track record to back it up," she says.

8. Talk to your parents.

With parents still playing such an outsize role in so many millennials' financial lives, Jordan says parents and adult children should each make an effort to have open conversations about money. "Parents should take a proactive approach to shore up their own finances and teach children about responsible saving. Parents don't realize how much of a connection they're going to have; that conversation is really important, and they need to start early," Jordan says. On the flip side, millennials should also prepare to potentially assist their aging parents with money one day. "That's a conversation they really need to start having," he adds.

9. Keep things as simple as possible.

It's easy to feel overwhelmed with the various financial management choices you have, but the bottom line is that you need to save more and spend less to accumulate more wealth, says Erin Lowry, 26, founder of BrokeMillennial.com and contributor to the U.S News My Money blog. "Don't get so aggressive with paying down debt that you completely eliminate savings of any kind. Everyone should have at least $1,000 tucked away in an emergency savings fund," she adds. "The best way to shed the feeling of living on a tight budget is to cut spending while increasing your earning power."

That's exactly what she did: When she first moved to New York City in 2011, she was living paycheck to paycheck with a desirable but low-paying job in the entertainment industry. She picked up shifts at Starbucks, worked as a babysitter in her off-hours and severely limited her spending. Eventually, she created enough of a buffer that she could scale back her extra work (and catch up on sleep).

10. Always look for the next level.

Once you achieve a basic level of comfort with your savings and budgeting efforts, then it's time to tackle the next task. Perhaps it's fully filling your emergency savings fund, investing or opening a retirement account. "Don't get comfortable with your status quo," Lowry says. "Push yourself further by contributing another percent or 5 to your 401(k). Learn more about investing. Most importantly, set financial goals and make them specific."

For the past six years, Eliza Cross, a professional blogger and freelance writer in Denver, has put herself on what she calls a "money diet."

Not that she coined the phrase. "Money diet" is a term that's been around since at least the 1980s. For a stretch of time, maybe a week and often a month, you spend no money, except on essentials like groceries, gas and medicine. Unlike a food diet, where you want to lose pounds, the goal is to gain money. And if you do it right, Cross says, you should have more money than usual at the end of the month, and you may gain better financial habits as well.

Cross has been putting herself on a money diet every January, for all 31 days. She writes about it and commiserates with her readers on her blog, HappySimpleLiving.com.

And while Cross does it every January - "it's a good time of year when we're motivated to make changes in our lives, and a lot of us have been spending a lot over the holidays," she says - you can obviously go on a money diet any time. That said, some parts of the year are probably more challenging than others, such as the middle of summer, when you may want to do things like go on vacation, visit an old-fashioned ice cream parlor or take the kids to the water park.

It will help your cause if your family embraces the idea of a money diet. Cross is divorced and her oldest child is a grown-up, so that makes it easier for her than someone with an uninterested spouse and seven teenagers (although that hypothetical family would need the money diet more). Cross has a 13-year-old son, Michael, but so far, she says he has hardly noticed the extra-frugal periods.

Want to give it a try? Here's how to get yourself on a successful money diet.

Food means strictly groceries. You have to eat. But in the spirit of your money diet, you want to watch where you eat even more than what you eat.

"We don't pay extra for restaurant meals, takeout or pizza delivery," Cross says.

You'll also want to avoid buying a can of soda at the gas station. Try not to make eye contact when you pass kids selling candy bars for school. You also really shouldn't be going out for a cocktail with friends during a money diet, unless your pals are paying.

Visit your library. Before you yawn at what sounds like obvious advice, listen to Mike Catania, COO of the retail website PromotionCode.org. He is noticing a trend in which libraries allow you to check out things beyond books, CDs and DVDs.

For instance, Catania says, in California, "The Oakland Public Library lets you check out tools for DIY projects."

In fact, some libraries lend pretty unusual items. The Arlington Public Library, in Arlington County, Virginia, lends American Girl dolls out for a week. The Ann Arbor District Library in Michigan actually has a website titled, "Unusual stuff to borrow," and offers patrons the chance to check out things like telescopes and home-improvement tools like an indoor air-quality meter.

Even if your library doesn't offer anything unique to check out, you can get access to a lot of free entertainment.

Take on some part-time work. Or ask for extra hours. Or put in extra hours if you're on salary, assuming those hours will help you get ahead.

What's the rationale for working harder during your money diet? Well, you have less time to spend money.

Lamar Dawson, an account executive at a public relations firm in New York City, says he took on a part-time job on weekends in January 2014 to pay off student and credit card debt. First, he picked up cash by working in a Spider-Man costume for a toy store in Times Square, and then he became a host for an Italian restaurant, where he still works. And while he killed off his debt by December 2014, Dawson says the extra work inadvertently put him on a money diet.

"I found that it helped me save money because I wasn't at brunch with my friends, who were group texting me to come out for endless mimosas," he says.

Mystery shop. This is only practical if you plan, since mystery shopping gigs often take at least a few weeks to get set up. Nevertheless, what a great way to "cheat" and still completely be within your money diet.

Judy Williams, who works for an emergency fire and water restoration company in Saint Francis, Wisconsin, had what she and her husband called a "no-spend" month a couple of years ago.

During their money diet month, Williams was a mystery shopper, which is a part-time gig in which you're hired to go to stores or restaurants and pose as a customer (you make purchases, but the company hiring you reimburses you and often pays you a little extra).

"Not only did we get to eat out for free, I got paid to do so," Williams says.

Shop at home. Mystery shopping and working more is fine, but really, a money diet is more about notgoing out, since that can make you feel deprived if the temptation to spend is great. Instead, a money diet is a good way to get to know your home a little better.

You probably own a lot of things you never use, and this is a great time to start utilizing them, Cross says. "Use up the things we tend to hoard in our pantries, garages, medicine cabinets and closets," she says.

Did you discover that you have run out of soap or shampoo during your money diet? Those are essentials, and you can buy them without feeling guilty, but Cross points out that you might want to check first and see if you have some hotel soap or fancy shampoo that someone bought you a while back.

You can even grocery shop at home, Williams points out. During her money diet, she and her husband used many items they had stockpiled in the freezer.

Holly Wolf, based in Chester Springs, Pennsylvania, and the chief marketing officer at Conestoga Bank in Philadelphia, says she lives a frugal lifestyle and often does her grocery shopping at home.

"That mango barbecue that you had to have, figure out how to use it," she suggests. "Ditto for the pickled onions, the 10 pounds of ground chuck that was such a bargain, the frozen strawberries and the soup you froze a few months ago."

One of the side benefits of shopping in your own pantry or freezer, Wolf says, is that it should curb yourimpulse-buying the next time you're tempted to purchase something offbeat that you're not actually likely to eat.

And just as it's fun to window shop and find something you never would have dreamed of buying, you may end up making a similar "purchase" in your own home.

"One year, in my own house, I found a kit for insulating windows, and so I used that, and I wound up saving money on my energy bill," Cross says. "During a money diet, it's all about getting creative and using what you already have."

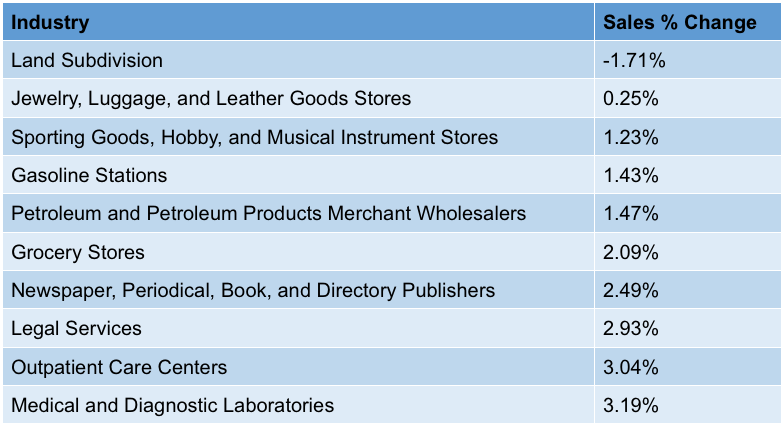

Looking for a business idea in a fast-growing sector? If so, you should steer clear of the industries below.

Sageworks has identified the industries that have experienced the slowest sales growth during the 12-month period ending October 23, 2015. At the top of the list is the Land Subdivision industry, comprised of companies dedicated to servicing land and subdividing real property into lots. Businesses in this sector have seen revenue contract 1.7 percent year over year. The bright side is, it's the only private company industry in the U.S. seeing negative revenue growth over the past year.

When an industry experiences contracting sales, a combination of internal and external factors are likely responsible, says Sageworks analyst Libby Bierman. Business owners witnessing a sales slowdown should take a close look at revenue models to determine problem areas, like underperforming locations or product lines.

In addition to land subdivision, retail is heavily represented on the slowest growing list. Retail industries included on this list were Jewelry and Luggage Stores, Sporting Goods and Musical Instrument Stores, Gasoline Stations, and Grocery Stores. Each of these four sub-sectors is growing revenues at an annual rate of less than 2 percent, compared to the average annual sales growth of 9.5 percent among all private companies.

One possible explanation for this slower rate of retail growth, of course, is the shift towards e-commerce and online retailers. Privately held brick-and-mortar retail companies are facing more competitive pressure than ever from online retail, as well as big box retailers.

"Even Amazon.com is becoming a common grocery store for some consumers," Bierman says.

The list also includes several industries within healthcare, such as Outpatient Care Centers and Medical and Diagnostic Laboratories. Inclusion on the list is far from a death sentence, however, as sales growth only tells part of the story, Bierman says. Without the context of other data, like net profit margin and previous periods' sales percent change, the most recent sales figures can be slightly misleading.

Legal Services is one industry where slow sales growth does not tell the full story, Bierman says. The growth may be slow but it is also consistent, and companies in this sector are much more profitable than the average private company.

Check out the table below for the full list of the slowest-growing sectors in the U.S.

Americans are increasingly whipping out plastic to pay for their purchases. This growing reliance on credit cards resulted in Americans closing out 2015 with more than $900 billion in credit card debt, according to a recent credit card study by CardHub.

That means the average U.S. household is shouldering the highest amount of credit card debt - more than $8,000 per indebted household - since the Great Recession.

It's a troubling (and disappointing) trend, especially when you consider just 18 months ago,many Americans reported either taking the scissors to their credit cards or making sure to pay off their balances in full each month. But more Americans seem to be practicing "swipe now, worry later" spending habits.

"Many consumers are focused on immediate gratification; it is very easy to pull out the plastic and make instant purchases," Laura Beal, a lecturer in finance, banking and real estate at the University of Nebraska at Omaha, told CardHub.

In addition to factors like income and financial literacy, CardHub said where you live plays a significant role in how well you manage your credit card debt and how high that debt rises.

According to CardHub, these 10 cities have the highest average credit card debt:

Beverly Hills, California: $13,583

Darien, Connecticut: $12,858

Westport, Connecticut: $12,220

Southlake, Texas: $11,512

Greenwich, Connecticut: $11,255

Highland Park, Illinois: $11,111

Colleyville, Texas: $11,107

Manhattan Beach, California: $10,721

Lake Forest, Illinois: $10,462

Calabasas, California: $10,444

These cities have the lowest average credit card debt:

Clarkston, Georgia: $2,705

Camden, New Jersey: $2,850

Coachella, California: $2,965

San Luis, Arizona: $3,028

Hamtramck, Michigan: $3,148

Delano, California: $3,150

Adelanto, California: $3,155

Laguna Woods, California: $3,300

Bell Gardens, California: $3,343

Lauderdale Lakes, Florida: $3,374

Here are some other interesting findings from CardHub's credit card debt study:

Based on residents' average credit card balance and income, College Station, Texas, has the longest estimated payoff timeline at 387 months (more than 32 years), which is 47 times longer than the shortest payoff timeline, 10 months, for Cupertino, California.

Americans added $21.3 billion in new credit card debt during the third quarter of 2015, which is 71 percent higher than the post-recession average.

Countless Americans ring in the new year determined to shed those few extra pounds around their midsection. But the new year is also a good time to sit down and take a good, hard look at your finances. Maybe you could add shedding debt to your list of New Year's resolutions?

If reducing your debt load seems overwhelming, just remember how great you would feel if you started 2017 with an extra $5,000 in your bank account.

First, take a look at your total debt. A recent NerdWallet study found that the average American household is shouldering $129,579 in debt - an alarming $15,355 of that on credit cards. That means the average American is forking over more than $6,600 each year in interest, roughly $2,600 of it for credit cards.

Yikes! But reducing the amount of money you're paying in credit card interest is sometimes just a phone call away, according to the New York Post,

"Few people ask a card company for a lower rate of interest," Matt Schulz, a senior analyst with CreditCards.com, told the Post. "However, if you have a pretty good payment record, we've found that most people who ask for it do get a lower rate."

Here are four more easy ways the Post says you can follow to get control of your finances and end 2016 with an extra $5,000 in savings:

Figure out where you're spending your money. Simply put, you need to compile a list of your expenses. "This sounds simple, but it's crucial: You need to know how much you make and what you spend it on. Then figure out what you can cut down on," Sean McQuay, a card analyst with NerdWallet, told the Post.

Spend less money. After you've compiled a list of your expenses, figure out where you can cut back so you can sock away some extra money in savings. For example, if you're spending $6 at Starbucks five days a week, you might want to start brewing your coffee at home instead. Cut back on eating out, pack a lunch and take it to work, and consider dropping your cable or downgrading to a cheaper cellphone plan. Check out "25 Ways to Spend Less on Food."

Make more money. "Freelance work, selling unused property or teaching classes online are some of the ways you can bring in some extra cash for paying down your debt," the Post explains. Paying down your debt means you're forking out less money for interest. (For more ideas, check out "20 Odd Ways to Make Extra Money.")

Create a realistic budget (and stick to it). Are there things you can reduce or eliminate from your budget? "Ask yourself: Do I really still need my cable subscription now that I'm on Netflix?" McQuay suggests. "Do I still need to have a landline phone? Do I still need that car I hardly drive? There are basic things consumers at any income level can do to increase their wealth." Check out "8 Secrets to Building a Budget You Can Live With."

According to the Post, those are four easy ways you can get a better grip on your finances and sock away up to $5,000 by 2017.

It's wintertime and that means it's time to hit the slopes. But as a lot of us know, planning a ski trip can quickly add up. Luckily, there are a few ways to enjoy that fresh powder without putting a dent in your savings.

First, renting skis at the lodge is costly and renting day of is even worse. So, if you don't already own skis, get them from a third-party rental house to save up to 30 percent off. If you have to rent from your lodge, try to reserve your skis online at least 48 hours in advance, and you should see discounts of up to 25 percent.

Next, try to buy your lift tickets online for more savings. At Liftopia.com, you can save an average of 27 percent off your lift tickets. Alternatively, you can check out larger ski and sporting retailers, such as Sports Authority and Dick's Sporting Goods. And don't overlook big box stores like BJ's, Sam's Club and Costco for some great deals.

Finally, look for all-inclusive ski packages to get the greatest value. Lift ticket and lodging packages are often great deals. Many hotels and B&Bs in ski towns negotiate special deals with resorts to offer ski tickets for free or discounted prices. Typically, you have to schedule these packages well ahead of time, so look into this option early to find the best deals.

Before you go on your next ski trip, remember these tips. You'll see that with a little pre-planning, going skiing doesn't have to be a slippery slope for your savings.

If you feel like you're getting nickel-and-dimed these days, you're not alone. But you may be paying for products or services that are available for free - no wallet necessary.

Here are six things you can get for free:

Wi-Fi (outside your home): If you're like most people, you pay for Internet service at your home, but that's the only time you should have to fork over your hard-earned cash for Wi-Fi because you can probably tap into a free connection somewhere else. Your local library provides free access, as do a number of businesses, including Starbucks and McDonald's. Another option to sniff out a Wi-Fi connection is to use a hotspot database like WeFi.

Books: Your public library is a great spot to check out books for free, either the old-fashioned way or as a digital download. I read lots of free downloaded books from Amazon. Though some books require that you're an Amazon Prime member, there are others that are offered for free through promotions. Project Gutenberg offers more than 50,000 free ebooks, including "Anna Karenina," "The Adventures of Sherlock Holmes" and "Jane Eyre," which you can read on your computer or your smartphone. Check out this article on how to get millions of books and magazines for free.

Water: Sure, you can buy expensive bottled water, but chances are it's no better than the water you get from the tap. So save yourself some money and ditch the spendy bottled water. If the taste or quality of your tap water really is bad, you may want to purchase a filtered pitcher or a faucet filter.

Credit report and FICO score: You can get a free copy of your credit report once a year by going to AnnualCreditReport.com. There are also now a handful of ways you can check out your FICO score - which is often used by lenders, bankers and landlords - free of charge. Many credit card companies provide their customers with a free copy of their score. According to the Consumer Financial Protection Bureau, you can also get access to your FICO score from a nonprofit credit counselor. Read this article for more on how to get a free look at your FICO credit score.

News: The Internet forever changed how people read or watch the news. You can get free news online 24/7. If you don't have Internet service at home, just head to the public library (or anywhere with free Wi-Fi) and you're set.

Banking: There are few things that Americans hate more than banking fees. You're less likely to run into pesky (and expensive) fees for banking services at smaller banks, like credit unions, online banks and community banks. Taking advantage of electronic features and direct deposit also sometimes allow you to avoid bank fees. Find more tips on how you can avoid paying banking fees here.

Are you paying for the items you see on our list? What everyday items or products do you get for free? Share your tips below or on our Facebook page.

Conventional wisdom says that you should never close a credit card account unless you have an overwhelmingly pressing reason to do so.

It's true that closing an account can hurt your credit. If you close an old account, it can shorten your credit history, which can then lower your overall credit score. Also, closing an account means that you have less credit available, so the balances you do have will take up a larger percentage of your available credit. This is called your credit utilization ratio (an important factor in your overall credit score), and you want that percentage as low as possible.

This doesn't mean that you should never close a credit card. Instead, it means that you need to be smart about which accounts you close and when you do so. Here are a few times when it makes sense to consider closing a card. (See also: How to Use Credit Cards to Improve Your Credit Score)

1. Preventing Identity Theft

The more credit cards you have, the greater the danger that one will be compromised and you'll have to deal with identity theft. If you have a card that has been stolen or are anxious about identity theft, consider closing one or more cards to reduce your risk.

The accounts most at danger are the ones you don't use very much. If a thief can get hold of one of these numbers, often by compromising a website where you used the card to make a purchase a long time ago, they can sometimes put quite a few charges on the card before getting caught. If identity theft is a worry for you, think about closing these infrequently used accounts first. An even better alternative: Avoid identity theft in the first place by practicing good credit card safety measures, such as only purchasing on secured, trusted sites using secure Wi-Fi.

2. High Interest Rates or High Fees

Cards that cost you money, especially when you aren't getting anything back, can be good candidates for closure. Sometimes, the benefits of a particular card (like one that earns you airline points) can be worth the annual fee. However, many people pay more in fees and interest than a card is worth.

Before you close a card because of what it costs you, try negotiating with the company. It never hurts to ask for a lower interest rate or a waived fee. The worst the company can do is say "No," and then you can go ahead and close it.

3. You've Already Made Your Major Purchases

If you're planning a major purchase that will require financing, like a car or a home, wait until that is complete before you cancel any credit card accounts. Since your credit score is almost sure to be at least a little bit higher with the cards contributing, it makes sense to wait to cancel them.

Even if canceling your cards won't hurt your credit very much, it could earn you a slightly higher interest rate. While a quarter (or even a tenth!) of a percent may not seem like very much up front, it can mean that you'll pay thousands of dollars more over the life of the loan. That's not worth it!

4. You Have Too Many Cards

While it's generally true that leaving cards open helps your credit, having too many open, in certain scenarios, can actually hurt you. Credit cards are considered revolving credit, which is the worst kind to have. If you have too much, especially in relationship to other types of credit, your score may actually be lower than it would be without a card or two.

In addition, it seems likely that people who manually underwrite loans look negatively on having too many cards open at once. This is mostly anecdotal but, if you're going after one of these loans, it may be wise to close down some cards.

5. When You Can't Stop Spending

No matter how much it hurts your credit, you should shut down credit card accounts if having them open is a spending temptation that you can't resist. If freezing or cutting up your cards doesn't work for you, and there isn't another way to stop yourself from building up more and more debt, then cancelling the cards makes sense.

This is a last-ditch scenario, but I've known more than one person who faced it. Desperate times call for desperate measures, and sometimes it's better to take the credit score hit rather than continue out-of-control spending.

Have you ever cancelled a credit card? What made it worth the hit to your credit score?

Whether or not yoga is your thing, you're probably familiar with it. The practice of yoga has become popular enough that most people know how yoga is done and how to do the basic poses.

What you may not know is that you can learn a lot about life in general while holding a pose like downward dog or happy baby. When you practice, you study not only the yogic postures, but also things like balance, flexibility, and mindfulness. And you can apply all of these concepts outside of the studio, too.

Here's how I've come to apply things I've learned from yoga to my personal financial life. I hope these ideas help you think about your money a little differently, maybe with a little more Zen! (See also: 4 Zen Concepts That'll Improve Your Finances)

1. Balance Is Central

My favorite yoga teacher will tell us to center ourselves not just over the left foot, but over the toes, or the heel. Slowly, I've come to realize that how I balance myself changes the posture subtly, often bringing in more of a stretch or making it more challenging.

Just as how you balance is key in the yoga studio, it's helpful when you're thinking about money, too. Most of us want more money, but what if we were to focus somewhere else? For instance, is there enough to pay the bills? Are we spending more thoughtfully than we did last year? And what would making more money actually add to our lives?

These questions, and more, can help us think in a more balanced way about our money. This, in turn, will free us to change spending or saving habits that might be harming us.

2. Proper Preparation Is Key

A good yoga teacher will prepare you for what is coming, both in the current class and in the future. There's a reason that harder poses often come near the end of a yoga class - it's because you wouldn't be ready for them before that. You have to open your hips, your hamstrings, your shoulders, and whatever else is needed for that final, challenging pose of the flow. If you don't prepare, you'll hurt yourself and hamper your ability to progress in the long term.

Money works the same way. What are your long-term financial goals? And your short-term goals? These aren't just going to happen. They require planning and preparation ahead of time. Just like in yoga, you need to do specific things now so you can reach your goals later. Want to travel around the world? Start saving. Need a specific kind of of mortgage, come spring? Look at starting the application now. Proper planning will help ensure your long-term financial health, just like a proper flow will help ensure that you stay healthy enough to continue practicing yoga.

3. Flexibility Is Crucial

Most people who practice regularly see an increase in their flexibility. And people like me - who just thought they weren't flexible at all - begin to see how this rise in flexibility influences their entire lives.

Similarly, the more flexible you can be with your money, the better prepared you'll be financially. Financial flexibility has to do with your ability to change how you spend based on your current circumstances. If you empty your emergency fund because your car breaks down, can you flex for a few months until the fund is replenished? And if you realize you need more than you'd anticipated for a down payment, can you find the funds and flex on a few things until you've made up the difference?

Financial flexibility pertains to small things, like how much coffee you buy and how often you dine out. But it also pertains to bigger things, like when you decide to buy a house, how you structure your investments, and more. Just as flexibility and strength are tied in yoga, they often come together financially, too. And you want your money to be as strong as it can be.

4. Self-Care Is Always Worth It

People start yoga for all different sorts of reasons, but they often continue because of self-care. Doing yoga feels good. It makes your body feel better, even alleviating long-term aches and pains. And it's often meditative, offering quiet and space that most of us don't have in our daily lives. So, in learning yoga, we often stumble onto self-care, too.

Learning self-care through yoga often helps people take better care of themselves financially. This can mean spending money on things - even little things - that make you feel good. A sweet smelling candle, a good book, or a cup of coffee can all be acts of self-care. It can also mean using more discretion about how you spend your money, so that you aren't always worrying about debt, overdraft fees, and how to pay the bills. Once people get started on a path to self-care, it often spills into their entire lives.

5. Mindfulness Will Help You Reach Your Goals

Mindfulness means staying aware in the present, and is often stressed in the yoga studio. Living in the now, paying attention to how your body is moving, what you need to do, and how to stay in a pose, can all help you learn to remain present - even when so many things pressure you to think about them, instead.

More than anything else, mindfulness is a path to self-mastery. It teaches us to choose where we focus, rather than letting the mind run willy nilly wherever it wants. And when we learn to focus in yoga, we learn a skill that can help us financially, too.

Being mindful - and therefore a master of ourselves - can help us stick to a budget. It can help us save up for something we really want. It can help us get through a frugal season without taking on debt. And it can even help us buy Christmas presents, because it will help us focus on the recipient and what they want, rather on everything we might like to buy for them. In the end, being mindful will help us save more, invest better, and be happier with what we have.

When we are open, willing learners, yoga can improve not only our physical health, but our financial health as well.

In America, we're known for our indulgences - home appliances, electronics, vacations, cars. So how does our spending stack up against Europeans, or folks in Asia? Read on for our analysis of the most uniquely American spendings habits out there.

1. The Lottery

Americans spend more money playing the lotto than on books, video games, and movie and sporting event tickets combined. In 2014, lottery spending in the U.S. totaled a whopping $70 billion. (See also: 6 Ways of Improving Your Lottery Odds)

2. Doctors and Dentists

The U.S. spends more public dollars on healthcare than all but two countries. There are a couple of reasons for that. First, healthcare services are notably higher in the U.S. than in most other nations. And secondly, Americans are greater users of expensive medical treatments and technologies, such as MRI machines.

3. Housing

Americans spend more money on housing than people in Canada, the United Kingdom, and Japan. In a 2009 study, Americans funneled an average 26% of their expenditures toward shelter.

4. Taxis, Planes, and Trains

The same study showed Americans also spend more on private transit, other than automobiles, than folks in Canada, the United Kingdom, and Japan.

5. Education

The U.S. spends more on education than any other developed nation, and most of the funding comes from the pockets of parents and private foundations. Total spending per student in the U.S. tops $15,000. For perspective's sake, Switzerland spends nearly $15,000 and Mexico pays about $3,000. Despite big spending, American students still lag behind comparable nations on international tests.

6. Prescription Drugs

Americans spend far more on prescription drugs - almost $1,000 per person per year - than residents of any other country. For some perspective: Americans spend 40% more than the next highest spenders, Canadians.

7. Politics

Americans spend more on political campaigns than any other country. To compare, India spent $5 billion in its last general election. That's one billion dollars less than Americans spent in the 2012 general election.

8. Tourism

When traveling abroad, Americans outspend vacationers from most other countries. In 2014, Americans abroad spent $112 billion - more than Germany, the United Kingdom, and Russia. The big out-spender, however, was China. Chinese abroad spent $165 billion that same year.

9. Christmas

Americans are more likely than residents of any European nation to go into debt to pay for Christmas presents. One in five Americans used credit to cover holiday spending in 2014.

10. Chocolate Bars

The U.S. leads global spending on chocolate bars, topping out at nearly $3 billion per year. That shakes out to an average annual chocolate expenditure of $57 per American.

A new year is here. And even if you've already broken the resolutions you made at the end of the holiday season, it's never too late to make new ones, especially when it comes to your finances.

Here are eight financial decisions you can make now that you'll never regret. Make the moves on this list soon, and you'll dramatically increase your odds of a happy financial future.

1. Save More for Retirement

How much money will you need each year to enjoy a happy and healthy retirement? That depends on what you want to do after you leave the working world. You'll need more money if you plan to travel the world, and less if you envision days spent reading, binge-watching TV, and playing with your grandchildren.

A survey released last April by the Employee Benefits Research Institute suggests that more workers understand they'll need large amounts of money to enjoy their retirement years. The survey found that more than one in 10 workers think they'll need to save at least $1.5 million for their retirements.

That's a lot of money. One way to reach such a lofty goal? Put away as much as you can each year now, even if your retirement days seem far away.

You'll never regret your decision to maximize your contributions to your 401K plan or your annual deposits to an IRA. Start boosting those savings today.

2. Building an Emergency Fund

What happens if your furnace conks out today? What if your car's transmission needs to be replaced? If you're like too many people, you'll put the cost of replacing these items on your credit card, building your debt.

The better option is to draw from an emergency fund of cash that you have already saved, usually in a savings account. Financial experts recommend that you build an emergency fund that can cover at least six months of your daily living expenses. (See also: 6 Emergency Fund Myths You Should Stop Believing)

This might seem daunting. But if you deposit what you can each month - even if it is as small as $100 - that emergency fund will steadily grow.

3. Pay Off Your Credit Cards

Carrying a balance on your credit cards each month is a terrible financial decision. That's because cards come with such high interest rates - sometimes 18% or more. This makes your monthly debt grow by too much, even if you don't add any new purchases to your cards.

Don't just make the minimum monthly payment on your cards. If you do this, it will take far too long to pay off your credit card debt. Say you have a credit card with a balance of $5,000 and an interest rate of 18.9%. If your minimum monthly payment is 4% of your outstanding balance, it will take you more than 11 years to eliminate this debt, even if you don't make any new purchases with this card.

The better move is to always pay more than the monthly minimum. And don't buy items with your cards that you can't afford to pay off at the end of every month.

4. Pay Your Bills on Time Every Month

A single missed payment - on credit cards, mortgage loans, auto loans, and other debts - can drop your three-digit FICO credit score by 100 points. That missed payment will also stay on your credit report for seven years.

Decide today to never make a late payment again. Having a low credit score makes it difficult to qualify for loans or credit. When you do qualify for these loans, you'll be faced with high interest rates.

5. Buy a Home That You Can Actually Afford

It's tempting when home shopping to stretch your budget to get into a bigger, more expensive home. But buying a home that's out of your budget, even by a bit, can be a big financial mistake. Those monthly mortgage payments can quickly become a burden.

Instead, buy a home that you can comfortably afford, even if it's not your dream residence. Mortgage experts recommend that your total monthly housing expenses, including your estimated new mortgage payment, be no more than 30% of your gross monthly income. Follow this guideline if you don't want to feel the strain each time your monthly mortgage payment comes due.

6. Track Your Spending

You might be surprised by how much you spend each month on take-out lunches or morning coffee runs. But if you create a spending book and track those expenses, it might help you make lifestyle changes that can add up to big savings each year.

A spending book is just a notebook in which you record all your daily purchases for a set period of time, usually anywhere from two weeks to two months. Once you're done tracking your expenses, add them up. This gives you an idea where you are overspending. (You can also use automated tracking at free sites like Mint.com.) If you're spending too much on those morning coffees, for instance, you might decide to limit your time at Starbucks to twice a week instead of five times.

7. Create a Household Budget

You might shudder at the thought of drafting a budget for your household. But you can't get control of your finances if you first don't know exactly how much money is coming in and going out of your home each month. Fortunately, creating a budget isn't difficult.

First, write down the income you receive each month. Then write down those monthly expenses that never change, everything from your mortgage payment to your auto payment to your student loans. Then, write down those payments you make each month that fluctuate a bit. This would include your utility bills, credit card bills, and transportation costs to and from work. Estimate these. Finally, include estimated amounts for monthly groceries, entertainment, and eating out.

Once you have these figures, you can determine how much money you should have left at the end of the month. Armed with this information, you can figure how much money you can save, invest for retirement, or put away for a child's college education.

8. Save First, Then Buy It

You want that new computer or that high-end flat-screen TV. It's tempting to simply use your credit cards, but the better move is to save up for that big-ticket non-necessity, and only buy it when you can pay for it with cash.

This takes patience, of course. It might take you several months to save up for that new TV. But you'll enjoy your new electronic treat more if you don't have to dread next month's credit card bill.

Landing a management consultant position at a top firm right out of college can result in a salary package topping $100,000 for the best employees - and more than $200,000 for recent MBAs.

But the first step toward securing such a coveted job is acing the internship. And at many prestigious consulting firms, interns are well compensated from the get-go - especially if they're working on their MBAs.

Management Consulted, a company that helps candidates land consulting jobs, compiled data on some of the top-paying firms for interns. To determine these figures, it culled through information from clients, spoke with industry insiders, and pored over real offer letters from readers.

With typical internships lasting 10 weeks or more, Management Consulted found that undergraduates can expect to make in excess of $1,000 per week. Meanwhile interns working on their MBAs often command more than twice that amount.

Compensation for consulting interns

But just how much of your earnings should you set aside for retirement and other savings to ensure lifelong wealth?

For one self-made millionaire, the magic number is 20%.

"Today, my wife, Michelle, and I each strive to pay ourselves the first 20% of our gross income," writes David Bach, who became a millionaire by age 30, in his book "The Automatic Millionaire."

"That may sound like a lot, but because I've worked up to it gradually over the course of fifteen years, it's become our 'new normal.'"

It took a while for Bach to grasp the idea of paying himself first: "When I first heard about this concept I was doing what most people do - trying to budget, beating up on myself for failing, and then scrambling at the end of the year to find some money to put in my retirement and savings accounts, only to find another year had come and gone and I had not made any financial progress," he writes.

Even when he did start setting aside money, it was a mere 1% of his paycheck, he says: "I was in my mid-twenties, and I wanted to make sure it didn't hurt. Within three months, I realized that 1% was easy, so I increased the amount to 3%."

Over time, he's gradually increased his percentage - from 3% to 10% to 15% - until he reached 20%.

He says anyone - no matter your income - can put money aside and let it accumulate. You'll learn to live without it, Bach assures: "If you are not paying yourself first now, that's probably because you think you can't afford to ... But I can tell you from personal experience that once you decide to pay yourself first and then you make it automatic, it's done - and within the first three months, you totally forget about it. You'd be amazed how effortlessly you can learn to live on a little less."

If you're only comfortable with setting aside 1%, it's better to start there than not get started at all. "This one little step will change your habits and make saving automatic," writes Bach. "And that will put you on a path that ultimately will make you rich."

Drugstore chains such as Walgreens or CVS frequently can't compete on price with stores such as Wal-Mart, Target or the local grocery store. But as with many things in life, there are hacks that level the playing field.

For example, WildForWags and WildForCVS owner Christie Hardcastle told me she regularly finds deals at chain drugstores that beat the pants off big-box and grocery stores. In fact, she claimed to routinely get things free, and sometimes even came out money ahead.

Impossible? That's how it sounded to me. So, I invited her to meet me at a local Walgreens and explain how she does it. This video is what resulted. Check it out, then read on for more.

As you saw in the video, you can sometimes get a good deal at places such as Walgreens and CVS just by keeping an eye out for ad circulars and in-store signs revealing what's on sale.

But to get the best deals, you'll have to do more - join loyalty programs and look for coupons, both store and manufacturer - and check out sites such as Christie's for ways to get the best current deals.

While that may sound like a hassle, the rewards are powerful: very cheap and sometimes free stuff.

I asked Christie to expand on the tips she offered in the video. For those of you new to the drugstore discount game, here in her own lightly edited words are some of her favorite products to purchase at drugstores:

1. Cereal

This is one of the items drugstores price below grocery stores to get you in the door. Each week, you'll normally see a different cereal brand or selection on sale. If you aren't brand-loyal, you can pretty much bet on getting a great deal every week.

If you have a brand you prefer, you'll usually see sales every six weeks or so. Plus, there are often coupons you can print even if you're new to couponing or don't have newspaper coupon inserts.

Drugstores will often run sales on milk and eggs with savings up to $1 over grocery store prices. Dairy prices vary regionally, but keep an eye out for sales or special offers.

4. & 5. Toothbrushes & toothpaste

These items will often have pharmacy rewards (like Walgreens Register Rewards or Balance Rewards points) that can really lower the price. Combine points with coupons, and you should be able to grab toothbrushes and toothpaste free or very inexpensively every four to six weeks.

6. Makeup

If you're using drugstore brands, you'll usually get a much better deal at drugstores than at grocery or department stores. There are often rewards for these products that you can combine with coupons and sales to get fabulous deals.

We see buy-one-get-one-free or buy-one-get-one-half-off sales on cosmetics regularly. Plus, because of limited space, drugstores often have great clearance deals to make space for new makeup products.

Another tip: If your store has a beauty counter, always ask the beauty adviser there for coupons.

7. Personal care items

Soap, body wash and lotions can often be purchased very inexpensively at the drugstore. Look for sales, rewards and store coupons that you can stack along with manufacturer's coupons for these items.

8. Store-brand garbage bags

I love Walgreens brand (Nice!) garbage bags. The quality is excellent, and the regular price is very reasonable. I usually wait for a sale, when I can grab them for about half the price of brand-name garbage bags.

9. Drugstore-brand diapers

While not a user myself, I've heard great things about Walgreens-brand diapers. Look for the buy-one-get-one-free sale that happens a few times a year, and you can grab diapers for about 12 to 13 cents each.

Not only do drugstores have a great selection of hair color, they often run sales and rewards promotions. You can also find many clearance hair-color deals. Combine that with coupons, and you can easily get hair color kits from your favorite brands for about $2.50 to $3.50 a kit.

The bottom line

While surveys - such as those from the public service consumer resource guide Consumer World - offer evidence that drugstores charge for convenience, learning to hack prices with rewards programs, sales and coupons can turn those high prices upside down.

If you haven't tried it yet, do so soon. And if you need free help, there's plenty out there. For starters, check out Christie's sites:

Which deals have you found at the local drugstore? How about sites that help you save? Spread the word by leaving a comment below or on our Facebook page!

Drafting a picture-perfect budget is only half the battle if you want to keep your spending in check.

Following rules is the other half - and that can be challenging if you underestimate expenses or forget to incorporate a few pieces of the puzzle into your spending plan.

Here are some commonly overlooked expenses that can cause you to throw in the towel on your budget each month:

1. Auto maintenance and repairs

At some point, if you don't take care of your car, it won't take care of you. So be proactive in order to avoid costly repairs down the road.

If a mechanic brings a major problem to your attention, don't ignore it. Instead, get a second and perhaps third opinion. Then, take care of it.

Use a calendar to plan out your children's extracurricular activities. That way, you can set aside the funds needed to pay up when the amounts are due.

The same rules apply to family fun. Plan ahead and always remain on the lookout for cheap or free fun.

Furry friends have needs, too. And, sometimes, those needs aren't as cheap as you think. So don't forget to factor in the costs of routine care as well as doctor visits. Also, take a look at "28 Ways to Save Big Bucks on Pet Supplies."

Are you responsible for obligations payable quarterly, semiannually or annually? If so, it's best to divide the total by 12 to get the monthly amount. Then, store the funds away so you won't be caught off guard.

Examples of such expenses include homeowner association fees, alarm fees and subscription dues. If your HOA fee is $300 quarterly, $100 should automatically be set aside each month to take care of the expense when it arises.

5. Special events

Your lifelong friend has decided to tie the knot next month, or your child's friend from school is having a birthday bash. Do you have the funds on hand to cover the travel costs or go out and purchase a gift?

If not, you may have to borrow to make it happen. Or, you can respectfully decline to attend.

6. Health insurance

Monthly premiums for health insurance can be expensive, and that's before co-pays and deductibles.

To cover these costs, you can either go into debt and pay interest, or plan ahead and have money set aside.

7. Road trips

Do you have money set aside to cover an extra tank of gas if you need it? Make sure you do - you never know when you'll need to make a quick trip to tend to important business, or to check on a loved one.

8. Service calls

The water heater can suddenly die, or your furnace may go on the fritz. So make sure you tuck away money for these unpredictable failures.

9. Utility consumption

When temperatures reach extreme lows, you may crank up the thermostat to stay comfy and wind up overextending your budget. A better alternative: Find more cost-efficient options, as we discuss in "15

Perhaps you stop by the bagel shop to grab a bite to eat because you were running behind schedule. Or, you take a co-worker up on an offer to have lunch. If you don't have the funds available for extras, another category of your budget will take a hit.

What is the biggest drain on your monthly budget? Sound off in our Forums. It's the place where you can speak your mind, explore topics in-depth, and post questions and get answers.

It's wintertime and that means it's time to hit the slopes. But as a lot of us know, planning a ski trip can quickly add up. Luckily, there are a few ways to enjoy that fresh powder without putting a dent in your savings.

It's wintertime and that means it's time to hit the slopes. But as a lot of us know, planning a ski trip can quickly add up. Luckily, there are a few ways to enjoy that fresh powder without putting a dent in your savings.