Aetna (AET) will spend about $35 billion to buy rival Humana (HUM) and become the latest health insurer bulking up on government business as the industry adjusts to the federal health care overhaul.

The proposed cash-and-stock deal, announced early Friday, would make Aetna a sizeable player in the rapidly growing Medicare Advantage business, which offers privately run versions of the federally funded health care program for the elderly and some people with disabilities.

Humana has nearly 3.2 million people enrolled in Medicare Advantage plans, a total that falls just sort of market leader UnitedHealth Group (UNH).

The combination also would bolster Aetna's presence in the state- and federally funded Medicaid program and Tricare coverage for military personnel and their families.

The deal value totals about $37 billion counting debt.

Hartford, Connecticut-based Aetna announced its deal a day after the Medicaid coverage provider Centene said it will spend $6.3 billion to buy fellow insurer Health Net. That deal would help Centene expand in the nation's biggest Medicaid market, California, and give it a Medicare presence in several western states.

The federal health care overhaul is expanding Medicaid coverage in several states as it attempts to provide health coverage for millions of uninsured people. Meanwhile, Medicare Advantage has seen its total enrollment triple over the past decade to 16.8 million people.

"Government markets are the most rapidly growing aspect of the system," said Dan Mendelson CEO of the market research firm Avalere Health.

Friday's deal comes two years after Aetna completed another push into government business with the $6.9 billion acquisition of Coventry Health Care, which administers Medicaid coverage and offers Medicare Advantage plans.

Health insurers have been trying to consolidate for weeks in a fresh merger wave. The Blue Cross-Blue Shield carrier Anthem (ANTM) went public late last month with an offer of more than $47 billion for another insurer, Cigna (CI).

Cigna rejected that deal, but The Wall Street Journal, citing anonymous sources, reported Thursday that the companies were still talking.

Health insurers see several advantages to combining. These multibillion-dollar deals offer an infusion of new business at time when growth has slowed in the biggest part of their business, employer-sponsored health coverage. Plus more employers are opting to pay their own insurance claims and hire insurers to administer the coverage. That's a less lucrative line of work for managed care companies.

Big deals also allow companies to quickly diversify their products and cover more territory. They also improve their technology and can ultimately save money by combining the back-office functions of two companies and cutting overlapping jobs.

The impact on consumers can be murky and likely won't be felt for at least a year, because insurers have already finalized most of their plans for coverage that starts in January. A combination may lead to fewer choices and some price changes for consumers, depending on where they live and who already is in their market. A deal also may foster technology improvements that lead to things like better smartphone applications for pricing or finding health care.

Aetna's purchase price for Humana includes a combination of cash and stock worth about $230 a share, based on Thursday's closing price of Aetna's stock. Aetna shareholders would wind up owning about 74 percent of the combined company, and Aetna's leader, Mark Bertolini, would serve as chairman and CEO.

The combined company will cover more than 33 million people. Only UnitedHealth Group Inc. and the Blue Cross-Blue Shield carrier Anthem Inc. cover more. A combined Aetna-Humana would be the second-largest insurer by revenue.

Shares of Aetna and Humana closed at $125.51 and $187.50, respectively, Thursday. Markets were closed Friday for the July Fourth holiday.

The shares of both companies, like several other insurers, have soared to all-time-high prices this year. The price of Humana shares, in particular, bolted past $200 in May after The Wall Street Journal reported that the insurer was a takeover target.

Nati Harnik/APBuffett focuses on the long-term value of his investments, not the day-to-day fluctuations.By Jeff Rose

When you think of great investors, the name at the top of the list is Warren Buffett. His insights and ideas can guide you in your own efforts to build wealth. As you consider your retirement future, here are five takeaways from the Oracle of Omaha:

1. Invest for the long term. Many of us are short-sighted. We panic at every market crash or try to chase a quick buck. However, Buffett teaches us to invest for the long term. When Buffett buys a company, he thinks of the long-term value. He doesn't look for something that offers splashy returns in the short term. He looks for something with staying power.

When investing for retirement, you need to think the same way. You won't be able to buy up whole companies, but you can invest for the long term by buying the market through index funds, and then staying in for the long haul. Your future self will thank you.

2. Have a purpose. Buffett has talked about the importance of having a purpose. You need to have an idea of what you want to do that gives meaning to your life. Studies show that retirees often lose their health shortly after quitting, when they don't have something to look forward to each day. Think about what you want to do with your life during retirement, and make it a new stage, rather than an end.

3. Learn from the mistakes of others. There is no reason to repeat the mistakes of others. Instead, learn from them. Many people sold at the bottom of the market in early 2009. Those folks locked in their losses. If they had been willing to wait a few years, they would have seen tremendous gains instead. Don't panic just because everyone else is panicking, and pay attention to the mistakes that bring others down. When you learn from the mistakes of others, you are less likely to fall victim to them.

4. Don't invest in the exotic. Buffett has talked about how he keeps enough cash on hand to meet his upcoming needs, but other than that, he keeps his money working for him. But that doesn't mean that he's investing in exotic assets. Buffett stays away from gold and currencies, and he also avoided the complicated credit default swaps that he famously referred to as instruments of mass financial destruction.

You can be the same boring investor. Focus on stocks, using index funds, and you will be likely to build wealth over time, without the stomach-churning volatility and risk that comes with more exotic assets.

5. Don't worry too much about leaving wealth to your children. While Buffett has said publicly that he wants his children and grandchildren to live fulfilling lives, he isn't taking care of everything for them. Indeed, a large portion of his wealth is going to charity, not his posterity, when he dies.

You can learn a similar lesson. Don't be so worried about providing everything for your children that you neglect your own retirement. And don't be so concerned about leaving them a pile of money that you don't enjoy your retirement when it comes.

Jeff Rose is a certified financial planner, U.S. combat veteran and the founder of GoodFinancialCents.com.

Elaine Thompson/AP

It's a conundrum we all face when planning a trip: Should you buy your ticket early and maybe pay a little extra to get a guaranteed seat, or wait for a better deal to come along at the last minute? No matter what you choose, it seems like the price of a flight is always lower after you've already booked.

But there's a new study out that shows when it's the most effective time to buy airplane tickets. Below are some tips, including what day of the week to buy, that you can use to save money the next time you fly.

Book Early, but Not Too Early

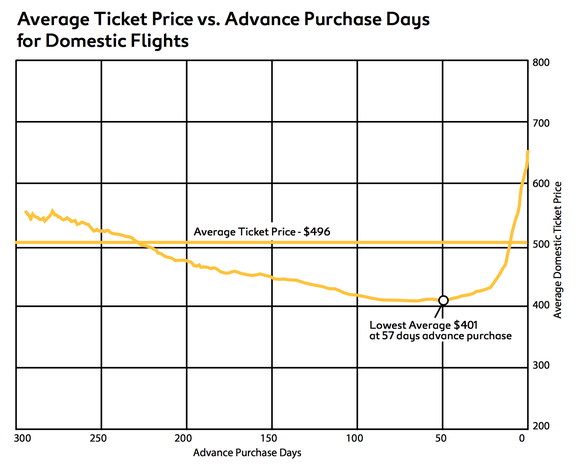

According to a recent report from Expedia (EXPE) called "Preparing for Takeoff: Air Travel Trends 2015," domestic travelers have a window between 50 and 100 days before a flight when airline tickets are cheapest. Booking too early or too late can result in ticket prices that are hundreds of dollars higher.

On average, the best precise day to book your flight is 57 days in advance.

Source: Expedia's "Preparing for Takeoff: Air Travel Trends 2015"

Booking in this optimal window can save you nearly $100 a ticket, on average, and the savings over booking last-minute can be as much as $250. So, plan ahead, but not too far ahead.

Interestingly, international travelers will want to plan much further in advance. Ticket prices tend to be lowest more than 100 days in advance, up to a year, for an international flight and climb steadily as takeoff approaches.

Source: Expedia's "Preparing for Takeoff: Air Travel Trends 2015"The Best Day to Book

There's also a strategy to what day of the week you should buy your a ticket. According to Expedia's findings, when booking in advance, you should try to book on a Tuesday. That's the day that can save you as much as $28 -- versus booking on Saturday.

At the very least, book midweek instead of on the weekend and you'll save around $20 on each ticket.

Knowing When to Plan Your Trip Is Half the Battle

There's no surefire way to know that you're going to get the lowest possible flight for an airline ticket, but following these tricks will ensure that you put yourself in position to get the best possible deal the next time you fly. Domestically, book 50 to 100 days in advance; internationally, book more than 100 days in advance; and book your flights midweek instead of on a weekend.

Getty Images

Gwen Thomas started preparing her son for college when he was just 13. Today, after helping him net $500,000 in scholarships for a higher-education experience that spanned some 30 countries, she teaches other parents how to get help sending kids to school.

Talk about a smart business idea. According to the College Board, the average cost of tuition and fees for the 2014-2015 school year was $31,231 at private colleges, $9,139 for state residents at public colleges, and $22,958 for out-of-state residents attending public universities. And that's for just one child.

For my wife and me, parents of three fast-growing kids and living month-to-month and check-to-check, our best hope of getting them through school is to be like Thomas and help our children chase the right mix of scholarships.

The (Green) Paper Chase

Replicating even a portion of Thomas' success won't be easy. The key appears to be spending the time and effort required to unearth good opportunities, and then applying for all of them. Here are her three tips for college-bound students seeking financial aid:

Start early. Thomas says she began getting her son into various leadership programs at age 13. She also advises parents to assess their children's "strong suits" and place them in programs that allow for unusual extracurricular success, whether that's sports, art, music, or making a significant contribution in a church youth group.

Serve often. A service mindset is particularly important for those looking to win top dollars. "Gone are the days that committees simply want academics," Thomas says. "Instead they want to see the grades and the gas spent on getting kids involved in service and volunteering."

Leverage the law of large numbers. Thomas started looking into scholarships when her son was in 11th grade. By the time college came around, he had applied for 100 merit scholarships and won 25. The more you apply for, the more likely it is you'll get the financial aid you need to send your child to a good school.

Where You Get Money Matters

Yet it's also not that simple. Scholarships not only vary in size but also duration. For example, a club or credit union that issues new scholarships every year may only grant awards for the school year in which they're won. Renewing the funds may require reapplying.

To get the best results, you'll want to first calculate your Expected Family Contribution, or EFC, which roughly equates to your estimated out-of-pocket for sending your student to college. Merit-based aid tends to reduce qualifying needs-based aid on a dollar-for-dollar basis, sometimes without zeroing out the EFC. Getting your estimate may help to develop a strategy for chasing an equitable mix of needs-based and merit-based aid.

Calculate your EFC here using the handy online tool provided by the College Board, and then make an appointment with the financial aid office at the college your child wishes to attend. They'll help you understand how the award could impact an overall aid package, says Jodi Then, education advisor at American Student Assistance's College Planning Center.

For those who don't yet know where they'll be going to college, high school guidance counselors can also help with planning. Or, if you're more of a self-starter, good resources exist online from The College Board and information portals such as Peterson's.

Merit-based awards are generally a boon for the students who get them. Applying them properly can mean the difference between getting the bulk of your education paid for and owing tens of thousands in tuition.

Although beer consumption has slipped in the United States, many Americans still enjoy cracking open a cold brew or two.

The share of Americans' total alcohol intake from beer dropped by nearly 10 percent from 2003 to 2013, while the popularity of wine and spirits has grown, according to 24/7 Wall St. But there are some states where beer continues to fly off shelves.

Using data from Beer Marketer's Insights, 24/7 Wall St. found that North Dakota residents are tipping back the most beer (43.6 gallons in 2013) per drinking-age adult in the country. At the other end of the beer-drinking spectrum is Utah, where drinking-age residents consumed a modest 19.6 gallons each in 2013. Low population density was correlated to greater beer consumption rates, 24/7 Wall St. observed:

"All but three of the 11 states with the highest beer consumption were less densely populated. [Eric Shepherd, executive editor at Beer Marketer's Insights] suggested there may be fewer entertainment options in rural areas. Not only that, but beer may also be among a shorter list of available beverage options in rural states compared to more urban states."

North Dakota: 43.6 gallons per drinking-age adult in 2013.

New Hampshire: 42.2 gallons.

Montana: 40.5 gallons.

South Dakota: 38.2 gallons.

Vermont: 35.9 gallons.

Wisconsin 35.8 gallons.

Nevada: 34.9 gallons.

Maine: 34.8 gallons.

Nebraska: 34.1 gallons.

Mississippi: 33.2 gallons.

"High per capita beer consumption in a state does not necessarily mean residents drink excessively," 24/7 Wall St. noted. Though the number of people binge drinking is usually elevated in bigger beer drinking states, as is the rate of heavy drinking.

I was disappointed -- though not surprised -- to see my home state of Montana on the list, not so much for the drinking but for its drinking and driving. Nationwide, less than 2 percent of American adults admitted to drinking excessively, then getting behind the wheel, 24/7 Wall St. said. In Montana, that number jumped to 3.4 percent, the highest percentage nationwide.

It's hardly a surprise then that Montana also has the second most deaths from alcohol-related car crashes in the nation (behind North Dakota).

Getty ImagesCreating a detailed financial plan is an essential step to retiring early.By Kelly Campbell

Retirement is thought of as the time to stop working, start slowing down and do nothing but relax. For many, however, it is becoming a time for more activity. In fact, many retirees are doing things they never thought possible, like training for marathons, traveling the world and even starting their own business. Retirement as we know it has changed.

And while our activities in retirement have changed, so has our retirement timeline. Many people see this new life as a destination. People thought of leaving their jobs with the sense of retiring from something. But with this newfound inspiration, people are now retiring to something, which means many want to get there as soon as possible.

But retirement still takes resources, and you must be prepared. And to pursue an early retirement, you must have a financial plan. You need to put numbers to paper, spreadsheet or retirement calculator. This is one of the most important steps you should take before you quit your job early.

The financial plan will look at all of the variables including rates of return, inflation rates, spending patterns, taxes and even unexpected expenses. Once you put all of this information into a retirement calculator, you can then adjust things to see if you will make it without running out of money. I suggest you run your plan as we do for all of our clients, out to age 95. That way, you will likely run out of air before you run out of money. That's an important part of your planning.

The beauty of the plan is you can forecast positive events, like having good investment returns, or some of the negative events, like a long-term illness. This type of planning should be done by anyone looking to retire.

When you have your plan, you can begin to take into account the things that may allow you to retire early. Here are five things you can do now to make that happen:

Downsize. Often, people's largest expense is their house. Going into retirement with a large mortgage payment is not a good idea, as you can use up all of your income on home expenses rather than travel budgets. If you downsize to a smaller home where you end up with a small mortgage, or better yet, no mortgage, you might be able to leave your job sooner than you think.

Relocate. Many of our clients have thought about moving out of the area as one of their retirement options. This is a good idea because Fairfax, Virginia, is an expensive place to live. Houses are expensive, services cost more and you will even pay more at the pump. Moving to a more rural and/or lower-cost area can definitely help you realize your retirement dream earlier.

Several of our clients have moved to Tennessee, North and South Carolina, Florida and Arizona. These areas tend to have a much lower cost of living, so their dollars can be spread over a longer period of time.

Before you make this move, consider choosing the area where you want to live and rent a place for several months so you understand the lay of the land.

Use home equity. Many of our clients have homes that are worth hundreds of thousands of dollars. Relocating and downsizing are both good ideas. But things become exceptionally better when they have cash left over after selling their old home and buying a new one. We see this all the time, where people will sell their home in Virginia for $700,000 and buy a new home in Florida for $400,000. This difference (likely somewhere around $200,000 to $250,000 after expenses) is like "found" money and can be used for monthly income for years to come.

Work part time. Having something to do after you leave work is important for mental stability, physical exercise and stress relief. Working part time can help. Finding a great job in retirement doing something you really like to do that also brings in extra income can help you leave your full-time job early. If that new part-time employment fulfills your passions, it also keeps you physically, mentally and emotionally stimulated, which is a positive in your retirement life.

Retire abroad. Living in the U.S. can be expensive, especially compared to other countries. Moving to another country can seem like an outrageous idea, but more and more Americans are choosing this option as they hit their golden years. Many choose their new location based on cost of living. But make sure you also take into account how friendly the locals are to American residents as well as what kind of health care you will have access to. Otherwise, you may really enjoy both the new culture and the lower expenses.

Changing your outlook on retirement can have a significant impact on your happiness, especially if you are able to do what you love. But this takes planning. As you plan to potentially retire early, keep these five things in mind. You never know ... you might be able to enjoy your new lifestyle sooner than you think.

Kelly Campbell, certified financial planner and accredited investment fiduciary, is the founder of Campbell Wealth Management and a registered investment adviser in Alexandria, Virginia. Campbell is also the author of "Fire Your Broker," a controversial look at the broker industry written as an empathetic response to the trials and tribulations that many investors have faced as the stock market cratered and their advisers abandoned their responsibilities to help them weather the storm.

Astrid Stawiarz/WireImage

Plenty of stocks go up and down in any given week. The gainers inspire us to keep investing. The decliners keep greed in check while reminding us about the risks of the equity markets.

Let's go over some of last week's best and worst performers.

Investors that strapped on Fitbit's freshly minted stock during last month's IPO are the picture of health these days. Fitbit came up big on the week after some flattering analyst remarks about the pioneer of wearable fitness trackers.

The week kicked off with RBC Capital Markets initiating coverage with a bullish perspective, eyeing a whopping 83 percent in revenue growth this year. CNBC's Jim Cramer then had some kind words to say about Fitbit. Both feel that Fitbit will capably survive the arrival of the Apple Watch, arguing that there isn't as much overlap as you might think between the buyers of smartwatches and fitness bracelets.

Bassett Furniture (BSET) -- Up 21 percent last week

A better-than-expected quarterly report sent shares of Bassett higher. The furniture-maker and retailer with 92 stores pitching midpriced merchandise came through with a profit of 39 cents a share. Analysts were settling for net income of just 30 cents a share.

Consolidated sales soared 31 percent for the quarter since the prior year's period. An acquisition helped juice up those results, but even if you back out the purchase, you find a still robust 17 percent uptick in organic sales.

Chemours (CC) -- Up 10 percent last week

Sometimes a spinoff can unlock value in a corporate subsidiary. Chemours took off after being spun off by DuPont (DD). DuPont shareholders received one share of the freshly public performance chemicals subsidiary for every five shares owned of DuPoint. Chemours is a leader in titanium technologies, fluoroproducts and chemical solutions, and the market seemed to like the value in the stand-alone subsidiary in bidding it higher -- and parent company DuPont lower.

Ambac Financial (AMBC) -- Down 24 percent last week

Greece isn't the only country with a volatile debt situation. Puerto Rico is also on the ropes, and bond insurers with exposure to the island nation took a hit on the potential shortfall. Ambac joined the bond insurers taking a hit on the potential default, though Ambac made back some of its losses on Friday when it was reported that Puerto Rico did make its July bond payments.

Ballard kicked off the week by announcing the acquisition of Protonex in a $30 million deal, but the real dagger was the surprisingly weak pricing of a secondary offering. The struggling fuel cell specialist sold a little more than 8.1 million shares in the offering at a price of $1.60 apiece. That's not very encouraging when your stock began the week perched well above a price of two bucks.

It's been two months since Freshpet came under fire after reports on social media surfaced of Freshpet premium dog food containing mold. The negative attention resurfaced. There's no proof that this is a problem outside of the isolated cases, and there has never been a recall. However, it's never good for a brand that prides itself on high-end refrigerated dog and cat food to be seen as potentially dangerous.

WASHINGTON -- U.S. service firms grew at a slightly faster pace in June, as business activity and new orders increased.

The Institute for Supply Management said Monday that its services index edged up to 56 in June from 55.7 in May. Any reading over 50 indicates that services firms are expanding.

Steady hiring over the past year has fueled a consumer spending rebound from a winter slump. Many economists say the economy will expand at an annual rate of 2.5 per cent in the second quarter, after shrinking during the first three months of 2015.

This was a mixed but still decent report on the U.S. economy.

Still, the index's hiring component slipped in June to 52.7 from 55.3 in May, which indicates that the rate of job growth might slow.

"This was a mixed but still decent report on the U.S. economy," said Jennifer Lee, a senior economist at BMO Capital Markets.

The report corresponds with economic growth of around 3 percent annually in the second quarter, Lee said.

The ISM is a trade group of purchasing managers. Its survey of services firms covers businesses that employ 90 percent of workers, including retail, construction, health care and financial services companies.

The increase in the broader index points to increasing demand for services from consumers and companies. Business activity climbed last month to a reading 61.5, up from 59.5. The levels for new orders ticked up to 58.3 from 57.9 in May.

"The overall business outlook remains strong and performance in our market has been very good," one retailer said in the ISM's survey.

The majority of the 18 sectors in the survey expanded last month, although both construction and mining firms contracted.

What should you do if your summer internship is starting to feel like a dud - if you're bored, doing different work than you were promised or struggling to make ends meet on the low pay? Here are five of the most common ways internships hit the skids and what you can do if it happens to you:

1. Your internship is turning out to be mostly clerical tasks, but you were expecting more substantive work.

Some amount of clerical work is normal in most internships, and it's not uncommon for interns to come in expecting to do more glamorous work than what they end up with. The reality is that many internships offer you the chance to get work experience and exposure to your field in exchange for what can be, yes, drudgery. After all, you haven't proven yourself in the work world yet. Ideally, you will be given more interesting work if you excel at those boring tasks and do them cheerfully.

However, if you were promised types of projects you aren't getting, or if you're just going stir-crazy from too much filing and coffee-fetching, talk with your manager. Say you understand the need to do the work you've been doing, but that you also want to ensure that the summer is a learning experience for you. Add that you're hoping for the opportunity for exposure to more substantive work as well. And if you discussed specific projects during the hiring process, now is the time to mention those. Ask if it's possible to carve out time to learn about and contribute to other projects your team is working on.

2. You're not getting enough assignments, and you're bored.

Talk to your manager. Tell her you have a lot of down time, and ask what additional projects you can take on to keep you busy. Some managers take on interns without considering the time investment they'll need to make in generating and overseeing projects for them. You might have one of those types of managers, so ask whether there are longer-term projects you can take on that will keep you busy for a good chunk of time and won't require you to keep checking back for additional work.

You can also ask if you can offer to help others in the office when you have down time. If you get permission to do that, you might find that others are happy to fill your plate when your manager won't.

3. You're not getting much feedback or guidance on your work.

Be clear about what you need! When you're given an assignment that's unclear, ask questions. For example, you could ask if there are samples of similar work that has been done in the past that you could look at or for a clear description of what a successful end product would look like.

You could also consider having a big-picture conversation with your boss and explain that you're not always sure how to tackle your assignments. You could suggest having a weekly check-in meeting so that you have a set time to talk about what you're working on, ask questions and get feedback.

4. You're not included in meetings and discussions around the office, and wish you could be part of them.

In order to keep meetings short and focused, managers will often try to limit participants to a low number, often including only those with a deeper background in the issues being discussed or those with decision-making authority. So it isn't always appropriate to include extra participants - but including observers is another thing. Try framing your request as a desire to sit in and observe, rather than as a participant. For example, you could say: "Would it be possible for me to observe some of the website strategy meetings? I'd love to sit in to get more exposure to that work, just as an observer."

5. You receive an internship stipend, but it's not even covering your travel to and from work.

It's not unreasonable to ask for some assistance with expenses. It may or may not be in your team's budget to cover it, but it's not outrageous to inquire about it. Try saying something like this: "I'm finding that my stipend isn't fully covering my expenses getting to and from work each day. Would it be possible to get some assistance with those expenses, so that I don't lose money by coming to work?"

(One caveat here: It's always better to negotiate this kind of thing before you accept an internship offer. It's usually harder - not impossible, but harder - to change the terms of a job offer once you've already begun to work.)

Alison Green writes the popular Ask a Manager blog, where she dispenses advice on career, job search and management issues. She's the author of "How to Get a Job: Secrets of a Hiring Manager," co-author of "Managing to Change the World: The Nonprofit Manager's Guide to Getting Results" and the former chief of staff of a successful nonprofit organization, where she oversaw day-to-day staff management.

Nati Harnik/APBerkshire Hathaway Chairman and CEO Warren Buffett

OMAHA, Neb. -- Investor Warren Buffett has given more than $2.8 billion worth of Berkshire Hathaway stock to five charities as part of his plan to gradually give away his fortune.

Buffett, who is Berkshire's chairman and CEO, said in a news release Monday that he made his annual gifts last week.

Buffett has been giving away blocks of Berkshire stock since 2006 with the biggest share going to the Bill and Melinda Gates Foundation.

Buffett also gave Class B Berkshire shares to his own foundation and to the foundations run by each of his three children.

In addition to these major gifts that Buffett makes each summer, he also gives smaller blocks of stock to several unnamed charities each year.

Mark Lennihan/AP

NEW YORK -- Starbucks is raising prices again starting Tuesday, with the increases ranging from 5 to 20 cents for most affected drinks, the company said.

The Seattle-based company also raised prices nationally about a year ago.

A small and large brewed coffee will each go up by 10 cents in most areas of the country, Starbucks says. That would bring the price of a large coffee to $2.45 in most U.S. stores.

Some other coffee sellers are cutting prices. Last week, J.M. Smucker (SJM) said it would cut prices for most of its coffee products because of declines in future prices for unroasted coffee beans. In an emailed statement Monday, Starbucks (SBUX) said coffee costs are only part of its expenses, which also include rent, labor, marketing and equipment.

The statement said the company continually evaluates pricing to "balance the need to run our business profitably while continuing to provide value to our loyal customers and to attract new customers."

A representative for Starbucks, Lisa Passe, said the price increases are expected to impact less than 20 percent of customers. But that estimate is based on current purchasing patterns, which include more cold drinks given the warmer weather.

The price hikes mostly affect hot drinks, Passe said. That means the percentage of customers affected by the higher prices would likely rise as people start buying warmer drinks as the weather cools.

Prices aren't being raised on any food items, Passe said. Starbucks has been trying to get more customers to buy food items like sandwiches in hopes of driving sales.

NEW YORK -- U.S. stocks fell in a volatile Monday session as Greeks resoundingly backed their government in rejecting the austerity terms of a bailout and China implemented emergency measures to stop a selloff in Shanghai's market.

Greek Prime Minister Alexis Tsipras promised German Chancellor Angela Merkel that Greece would bring a proposal for a cash-for-reforms deal to an emergency summit of eurozone leaders Tuesday, a Greek official said. It was unclear how much it would differ from other proposals rejected in the past.

Equity futures tumbled at the open late Sunday after Greeks voted no to the terms imposed by its creditors. However the S&P 500 didn't fall more than 1 percent throughout the Monday session and even turned positive in morning trading.

Greece can't pay their bills, there's no middle ground there and other countries are going to have to foot the bill and they are angry.

Though Greece is causing a lot of uncertainty, a deal should get done to keep them in the eurozone, according to Karyn Cavanaugh, market strategist at Voya Investment Management in New York.

"Greece can't pay their bills, there's no middle ground there and other countries are going to have to foot the bill and they are angry," she said.

But more than billions in debt are in play as "Greece is the southern gateway to Europe. The strategic value is not being quantified."

The Dow Jones industrial average (^DJI) 46.53 points, or 0.3 percent, to 17,683.58, the Standard & Poor's 500 index (^GSPC) lost 8.02 points, or 0.4 percent, to 2,068.76 and the Nasdaq composite (^IXIC) dropped 17.27 points, or 0.3 percent, to 4,991.94.

Weighing further on investor sentiment, Chinese brokerages and fund managers vowed to buy massive amounts of stocks as Beijing unleashed an unprecedented series of support measures to stem a decline of nearly 30 percent in the main Shanghai index over the past three weeks.

"People see 'emergency measures' and they think 'that can't be good,' " said Voya's Cavanaugh.

The Shanghai index rose 2.4 percent overnight but a measure of Chinese stocks traded in the United States fell the most in 19 months, pointing to caution from investors outside of China about the effectiveness of the government's measures.

Energy Leads Drop

Energy stocks led the decline on Wall Street after U.S. crude futures prices settled almost 8 percent lower on concern over growth in China and the Greek uncertainty.

The S&P 500 energy index fell 1.3 percent, marking its fourth decline of more than 1 percent in the past seven sessions.

Health insurer Aetna (AET) fell 6.4 percent to $117.43 after it said it would buy smaller rival Humana for about $37 billion. Humana (HUM) closed up 0.8 percent to $188.96.

The deal is seen facing antitrust scrutiny, which could make other large-scale mergers in the sector more difficult. Anthem (ANTM), Cigna (CI), Centene (CNC) and Health Net (HNT), which are all in takeover talks, ended lower.

Declining issues outnumbered advancing ones on the NYSE by 1,946 to 1,132, for a 1.72-to-1 ratio on the downside; on the Nasdaq, 1,600 issues fell and 1,181 advanced for a 1.35-to-1 ratio favoring decliners.

The benchmark S&P 500 index posted 5 new 52-week highs and 32 new lows; the Nasdaq composite recorded 44 new highs and 130 new lows.

About 6.6 billion shares traded on all U.S. platforms, according to BATS exchange data, below the average of 7.6 billion in the past five sessions.

What to watch Tuesday:

The Commerce Department releases international trade data for May at 8:30 a.m. Eastern time.

The Labor Department releases job openings and labor turnover survey for May at 10 a.m.

The Federal Reserve releases consumer credit data for May at 3 p.m.

NEW YORK -- To lease or buy can be the biggest question facing someone looking for a new vehicle, especially these days, as lease rates keep creeping up to the highest rates in more than a decade.

There are excellent reasons for either. Those who lease always have a new car; those who buy can drive back and forth across the country with no worry their mileage allotment will be passed.

James Bell, head of consumer affairs at General Motors, says it boils down to what the prospective driver requires of a vehicle.

"Leasing vs. buying ultimately comes down to to the expected usage by the driver as well as their personal tastes and habits. Love that new car smell? Lease. The kind of person that enjoys maintaining a car for many miles? Buy," Bell says.

If you don't have the money for a large down payment or you want to get more car for your money, then leasing is the best choice.

Chris Naughton, regional manager for Honda Northeast, says finances can often be a deciding factor.

"If you don't have the money for a large down payment or you want to get more car for your money, then leasing is the best choice," he says, since a driver pays only for the portion of time a car is used.

"Lower monthly payments and less money down can make leasing seem like a great deal. The truth is that leasing offers a lot of convenience, but only if you are willing to put up with restrictions, which can include lower mileage limits -- typically only 12,000 miles a year, sometimes 10,000 miles a year -- diligent upkeep and care of the vehicle and, in some cases, penalties for early termination," says the folks at Kelly Blue Book.

End-of-lease costs can be a killer for those unaware of rules about the condition a car is expected to be when it's returned. What many people consider to be minor dings and dents may be outside what the dealer considers normal vehicle wear and tear, and the lessor could be penalized.

"The biggest surprise from leasing is potentially when the driver returns the vehicle to discover accessed fees for over-mileage or minor damage," Bell says. Drivers should be honest with themselves about how they drive, of course: A person who tends to park closely to another car or eats pizza while driving is likely to rack up damage penalties.

Potentially offsetting these costs is the fact that a leased vehicle is almost always under a manufacturer's warranty. This means the driver rarely has to pay large-out-of-pocket costs if something breaks.

Kelley Blue Book also advises reading all the fine print on lease paperwork. Lessors have a final decision to make at the end of a term, when the driver can decide to buy the car outright for a price set at signing.

"After a lease deal is offered to you, be sure to pay close attention to the negotiated purchase price of the vehicle and any additional fees outside the lease rate, and never sign a lease contract unless the residual value or optional purchase price at the end of the lease is clearly shown," the company says.

Despite the pros and cons of leasing vs. buying being almost even, about 70 percent of new-car drivers opt to buy -- interestingly a figure that is reversed when it comes to luxury vehicles. (Because a lease allows a person to "buy" more car, Naughton says.)

The nonprofit, member-owned financial institutions often have lower rates on loans and credit cards, higher rates on savings and fewer fees for checking accounts. To some, they also seem friendlier.

"I enjoy the small, personal touch that they give," says Ron Lau. Lau is one of an estimated 100 million members of the nation's 6,557 credit unions that hold more than $1 trillion in assets.

With so many choices, how do you pick the credit union that's right for you?

Compare rates and fees, of course, but you should check out these criteria, too:

1. Can I join? Anybody can join a credit union, but not necessarily any credit union. Each credit union serves its "field of membership," a common bond among members, says myCreditUnion.gov, the website of the National Credit Union Administration.

Eligibility may be based on:

Employer: Many employers sponsor their own credit unions.

Location: Many credit unions serve anyone who lives, works, worships or attends school in an area.

Family: Most credit unions allow members' families to join. So if someone in your family is a member of a credit union, you may be eligible, too.

Group membership: Church, school, alumni, labor union, homeowners' association are among groups that may define a bond.

For example, BECU in Washington state was founded in 1935 by 18 Boeing employees, but now it is 900,000 members strong, has more than $13 billion in assets and is open to all state residents and students attending Washington colleges and universities.

2. Does it offer services I need? Start with the basics, experts say: Make sure that your credit union offers home lending services, issues credit and debit cards, provides auto loans, features a good savings program, and offers financial counseling.

Are you looking for easy access to ATMs or branches nationwide?

"Because credit unions are not-for-profit, we cooperate with each other," Joyce Gaines, of Brightstar Credit Union, told Money Talks News financial expert Stacy Johnson. "Our members can go in other branches nationwide and access their accounts to make a deposit or withdrawal."

Unlike big banks, most credit unions don't have 24/7 call centers, so if that's important to you, ask if banking is restricted to business hours. Also, if you need it, see if the credit union offers mobile apps to view your account balances, pay bills, deposit checks and send money online.

Maybe you're looking for services such as investment, retirement and estate planning. Some credit unions offer personal finance help like their big-bank cousins, others don't. So be sure to ask.

3. Which is the best located? Online resources can help. MyCreditUnion.gov offers a tool that identifies credit union branches by ZIP code or city, shows which have drive-thrus or ATMs, and provides details including address, phone number and website. Similar tools are available from ASmarterChoice.org and regional credit union groups, such as Pennsylvania's ibelong.org. Most sites offer maps and directions to branches.

4. Will my money be safe? The National Credit Union Administration, with the backing of the U.S. government, operates and manages the National Credit Union Share Insurance Fund, insuring up to $250,000 for each member the deposits of all federal credit unions and the majority of state-chartered credit unions (many credit unions hold dual charters). Some state-chartered credit unions may insure their funds through private insurance companies.

Peer average ratio: How the credit union compares to federally insured credit unions of similar asset size.

Percentile rankings: How the credit union's financial performance compares to federally insured credit unions in its peer group.

Net worth: A capital level above 7 percent net worth is considered well-capitalized.

Return on average assets: Measures net income (or loss) in relation to average assets and represents the bottom line.

Delinquency: How many loans are late compared to total loans.

Net charge-offs: An important indicator of the effectiveness of lending and collection practices.

5. How do I get started? If you are eligible to join, you can easily become a credit union member by completing a membership application, depositing and maintaining the minimum par value of a share (generally ranging from $5 to $25), and paying a one-time membership fee if there is one.

Also, if you're moving your business from a bank, ask if the credit union can make transferring easy with a switch kit. The time-saving packet of forms and information guides you through the process of switching and may include direct deposit forms, worksheets and checklists.

As Stacy Johnson notes, credit unions are a great solution for many people, but you still need to shop around and ask questions before you decide where you want to have your money relationship.

What's your experience with credit unions? Share with us in comments below or on our Facebook page.

Like this article? Sign up for our newsletter and we'll send you a regular digest of our newest stories, full of money saving tips and advice, free!

Getty ImagesSpend less, save more and reduce your stress.By Tony Armstrong

If you slept in a bed last night, ate a meal today, wear clothing or drive a car, you probably agree that daily life can be expensive. The number of things you have to pay for can seem endless.

But what if you could cut back in a big way in one or two spending categories and get ahead on your financial goals?

Some intrepid savers have done just that, resulting in less debt, more flexibility to adapt to career changes and a nicely padded savings account.

Here's how you can follow their lead.

1. Go bulk or grow your own. Food is expensive, especially convenience foods and restaurant meals. The average American spends about $153 a week on food, according to 2013 data from the Bureau of Labor Statistics.

When Stephanie Swartz of Lakewood, Colorado, lost her job as a financial adviser, her ability to trim food costs came in handy. She buys food in bulk at Costco with her mother and sister to cut costs. The three have cooking parties and make dishes to freeze for later. "It saves a bunch of money," Swartz says. "I always have something in the freezer."

Some people take it a step further, growing vegetables or even raising farm animals at home. Johanna Fox Turner, a certified financial planner with Milestones Financial Planning in Mayfield, Kentucky, says her son and daughter-in-law have started raising chickens for eggs and are planning to keep a goat for milk. "They live a very low-cost lifestyle," she says.

2. Ditch the car. It costs Americans an average of $8,876 a year to own and operate a sedan that drives 15,000 miles annually, according to a 2014 study from AAA. You may be able to save a lot of money by getting rid of your car. Taking public transportation is a less expensive alternative to driving, and biking or walking has the added benefit of improving your health.

If you can't do without a car entirely, compare car insurance costs to make sure you're not overpaying. Find out if lowering your deductible or switching to a pay-per-mile plan can save you money.

3. Tailor your own clothes. "Over time, I taught myself how to sew out of necessity," Swartz says. She found a discount fabric store in Denver and keeps an eye out for inexpensive patterns. Her sewing skills also allow her to mend or repurpose older clothing.

"If you can't afford clothes, you have to fix what you have," she says. This approach has helped her cope with unemployment. "You have to look nice to go to an interview, but you can't spend a lot of money on anything before you have a job," she says.

4. Buy used. For some, frugality starts as a practical measure but becomes second nature. Amanda Folson, a product manager at PagerDuty in San Francisco, says a friend gave her the idea to buy clothes on eBay.

"Instead of paying $40 to $60 for a pair of jeans, I pay maybe $10," Folson says. Although she's buying pre-owned clothing, "more often than not, these are things that people haven't worn," she says. "They've usually got the tags on them."

Household goods like dishes and furniture can also be bought used, either through online auction sites like eBay or local Facebook groups, or by going to thrift stores and yard sales. In some cases, refurbished electronics cost less than brand new ones and still come with a warranty.

5. Embrace living with less. When Folson moved to San Francisco from Maryland, she decided not to spend the estimated $5,000 to move her furniture right away. She instead stored it at a relative's house. But nearly a year later, she's learned to enjoy having an almost empty apartment.

Folson has an air mattress, but usually finds it more comfortable to sleep in the hammock she strung up. Other than that, she doesn't have much besides computers, guitars and a bicycle.

"I like not having a whole bunch of stuff," she says. "My savings account really appreciates that."

Folson's thrifty ways allow her to put about $3,000 a month in her online savings account. And what's she planning to do with all that money? She's thinking of buying a condo or a tiny house -- a lofty goal for someone who is only 26 and living in the pricey Bay Area.

6. Make the most of your space. Smaller homes can save occupants on everything from rent to utilities to elbow grease -- they're much easier to clean and maintain. Cutting down on possessions can also make a modest-sized space more comfortable. Without furniture, Folson says her 700-square-foot apartment feels downright roomy.

Among Turner's clients, some with bigger houses have managed to pad their savings by renting out a room through online listings sites like Airbnb or VRBO. "In some cases, they can almost pay the whole mortgage," Turner says.

What to Do With Your Extra Money

Spending less can make life easier in many ways. Of course, not all money-saving measures require a radical lifestyle change. But for some people, changes in their spending habits have made them happier and less stressed. More money in the bank is only a side benefit.

Tony Armstrong is a staff writer at NerdWallet, a website devoted to helping consumers make smart financial decisions.

It's beginning to look a lot like Christmas! Wait, what?

As much as we complain when stores deck the halls while it's still beach season, it turns out that they might actually be on to something.

Although we've got months left till Christmas, believe it or not, the best time to start plotting out your holiday spending is now.

Because the more you plan ahead, the less likely you are to overdo it -- and the more likely you are to still have some jingle in your wallet when 2016 rolls around.

Don't believe us? A 2014 American Research Group survey found that early-bird holiday shoppers shell out almost $400 less than those who put it off until November.

So don't be a last second Santa -- get moving on these eight ahead-of-the-game holiday budgeting, planning and shopping to-dos.

Head Start To-Do No. 1: Hash Out Your Holiday Budget

Just as with any other financial goal, the first step to getting financially ahead for the holiday season is to nail down a budget.

One of the best ways to do that, says John Neyland, a financial adviser and president of JCN Financial & Tax Advisory Group in Baton Rouge, Louisiana, is to add up last year's holiday receipts and credit card charges for a clear picture of what you spent.

You can then use those numbers as the basis for creating a 2015 holiday budget worksheet, where you'll plug in realistic estimates for every holiday spending category -- from entertaining and gifts to travel and charitable donations.

Once you've landed on the right figures, devise a specific savings strategy that you'll execute over the next six months to cover those holiday costs -- such as brown-bagging your lunch a couple days a week and banking the difference.

Head Start To-Do No. 2: Open a Holiday Savings Account

Even if you're not quite ready to start your holiday shopping, it's never too early to start your holiday saving.

And while it may seem easier to simply funnel your holiday money into a catchall savings account that also includes your emergency cash, Neyland advises against it.

"Your emergency fund should be used for emergencies only -- I really can't stress enough how vital it is to keep that separate," he says. "Opening different accounts for each savings goal is a good way to keep from dipping into funds earmarked for a different purpose."

When shopping for a place to park your holiday cash, Neyland recommends looking at online banks, which typically offer favorable interest rates -- as well as provide an extra layer of protection against the temptation to withdraw the funds for other things.

"The easiest way to save money is to never see it in the first place, which is why you should also consider setting up an automatic transfer from your paycheck to your holiday savings account," Neyland adds. "The good news is that, by starting in July, you'll be able to take out a much smaller amount each pay period than if you wait until November [to set up an account]."

Head Start To-Do No. 3: Plot Out a Detailed Holiday Spending Plan

With a first draft of your holiday budget in hand, dig deeper by pinpointing exactly how you'll spend money within each category to ensure your numbers are accurate.

Is it your turn to host the annual cookie party? Then be sure to factor enough money into your entertainment budget to cover baking supplies and decorations. Do you need to buy plane tickets to visit family for Thanksgiving and Christmas? Bake that into the "holiday travel" section on your worksheet.

"Knowing who you want to buy gifts for -- and how much you'll be spending on each person -- is key. This way, you can start collecting a gift a month."

"Creating a plan well before the holidays not only keeps you organized, but it allows you to take advantage of deals throughout the year -- alleviating overspending when you're pressured at the last minute," Neyland says.

And don't forget to put advance thought into whose stockings you'll be stuffing.

"Knowing who you want to buy gifts for -- and how much you'll be spending on each person -- is a great way to stay organized," says consumer savings expert Andrea Woroch. "This way, you can start collecting a gift a month, or whenever you come across a sale or coupon, so you don't double up or waste money.

Head Start To-Do No. 4: Canvas Hidden Costs

Take some time to think about the sneaky expenses you've failed to plan for in past years -- such as a tip for your doorman -- and revise your spreadsheet as needed.

The beauty of this exercise is that you might find opportunities to save, too. "Some holiday expenses, like travel, might be non-negotiable -- but certain areas of your budget could have more wiggle room," Neyland points out.

Case in point: Do you usually end up paying rush shipping fees, or add on an extra $5 for in-store gift wrapping? Acknowledging these costs now can help you avoid them -- and keep them from busting your budget at the last minute.

Head Start To-Do No. 5: Hit Pause on One Habitual Expense

Let's be real: There's always room to scale back your budget a bit more.

Whether it's your tendency to toss a celebrity magazine into your cart at the supermarket checkout or to order several appetizers with dinner, choose one unnecessary expense you can live without -- and funnel the money saved into your holiday account.

"If it makes it easier to eliminate a certain luxury, remind yourself that this exercise is temporary -- although you might find you don't miss it as much as you thought you would," Woroch says.

Head Start To-Do No. 6: Suss Out Seasonal Sales

Since you're getting an early start to your holiday shopping this year, you'll actually be able to take advantage of seasonal sales.

Gift cards are great because you can use them as presents or stocking stuffers, or as a way to save on your own holiday expenses.

Want to buy Junior a new bike for Hanukkah? Start looking in January. Need some new kitchen gadgets in time for holiday hosting? They typically go on sale in October.

"Back-to-school sales are also a great time to find deals on winter wear items that will be perfect for holiday gifts, like boots or cashmere sweaters," says Woroch, who also recommends following retailers' social media accounts to source additional discounts.

Another shopping secret? You can nab gift cards at up to 90 percent off for such stores as Target, Home Depot, and GameStop on a site like GiftCardGranny.

"Gift cards are great because you can use them as presents or stocking stuffers, or as a way to save on your own holiday expenses," Woroch says. "For eight years straight, they've been the most requested gift item."

Head Start To-Do No. 7: Redeem Those Rewards

Between new summer duds for the family and upcoming travel reservations, you've probably racked up quite a few credit card points that you can put to good use for your holiday-centric spending.

"Eventually, points expire," Woroch explains, citing a well-known report that found at least $16 billion worth of rewards go unredeemed every year. "Banking them for the holidays is a great way to save on gifts and travel -- and avoid debt."

But before redeeming, do some research on your creditor's website to ensure you're not missing out on any valuable incentives.

For instance, Woroch says, some cards offer big bonuses -- like 25 percent extra cash back -- to cardholders who don't redeem their rewards until they've accrued $300.

And, of course, remember to only charge what you can pay off in full -- lest you end up triggering interest charges that will cancel out those rewards benefits.

Head Start To-Do No. 8: Track Your To-Do List

There's just one downside to all this proactive holiday planning: If you're not careful, you're likely to forget what you've purchased and buy it twice -- which is why organization is key.

Lisa Krecklow, 48, a medical device sales recruiter in Portland, Oregon, keeps her spending in check with the Better Christmas List app. It allows her to create groups of people she's exchanging presents with, juxtaposed with a list of gift ideas and her budget. She can also track each gift's status, like whether it's been purchased, wrapped, and even shipped.

"Having that information at my fingertips ensures that I choose gifts that fit my budget, and nothing falls through the cracks," Krecklow says. "As an added bonus, the gifts I don't buy can stay on the list as ideas for next year."

Woroch herself likes OneReceipt, an app that digitizes paper receipts on your phone and categorizes them, so they're easy to find when making returns and exchanges or logging your spending.

"You can often request that a retailer email your receipt, and then create a separate folder in your account for all your holiday purchases," Woroch says. "This will help you track your spending, gift purchases and even charitable donations -- and make it simple to access a receipt when you need it."

While it takes some initial effort to stay organized, your reward will come in December -- when you're sipping eggnog by the fire and others are duking it out at the mall.

NEW YORK -- Americans don't like so-called "robocalls" -- telemarketing calls from companies looking to pitch products and services, some of them with fraudulent intentions.

According to Consumer Reports, U.S. consumers have placed 217 million numbers do-not-call requests since the agency began tracking them, while telemarketing fraud costs Americans $350 million annually.

Still, companies manage to slip through the cracks and make robocalls, anyway. According to the Federal Trade Commission, the FTC receives between 250,000 and 300,000 consumer complaints a month against telemarketers, 60 percent of them directly linked to robocalls.

Shel Horowitz, a green business profitability expert, is one of those consumers who have a big problem with robocallers. "I especially get annoyed to see my own name and phone showing up as the call originator on my own caller ID, meaning they are probably poisoning the world against me by masquerading as me to others too," he says.

Other consumers say it's an uphill battle to block all robocallers, but there are some effective ways to keep annoying telemarketers at arm's length. "There really is no pro-active way to protect your home from robocalls," says Larry Peck, a consumer who is constantly battling robocallers. "Most companies who do them ignore the Do-Not-Call list anyway, and I'll call them back and get them to take me off their list."

"If they don't, I block them via Comcast's call blocking feature," he added. "I can also block their number on my actual landline phone too. As far as my cell phone, Verizon lets me block up to five numbers on a rotating basis. But the problem is, you're always dealing with robocalls on a reactive basis."

Job one for consumers looking to block robocallers is to sign up for the federal Do-Not-Call List which will prevent legitimate telemarketers from calling you, says Steven J.J. Weisman, an attorney and consumer fraud specialist based in Amherst, Mass. "Even if you are on the Do-Not-Call List, the law still permits you to receive robocalls from charities, politicians and polltakers," Weisman says. "However, whenever you receive any call, particularly a robocall, you have no way of knowing who is really calling you. So the best thing to do is to not bother to pick up the phone if you don't recognize the number - let legitimate callers leave a message and return their calls."

Consumers can download some handy mobile apps that can steer them clear of aggressive telemarketers, advises Keeon Rudder, a motivational speaker and global business consultant. "The easiest way to avoid spam calls is to download an app to hang up on such incoming calls," Rudder says. "I've found Mr. Number to be quite effective in thwarting unwanted callers."

Clair Jones, a home automation, Internet, and phone service expert with Localinternetservice.com, says the best thing you can do if you receive a robocall is to hang up immediately. "If you speak or push any buttons on your phone you are inadvertently indicating interest and signaling that you are a good target for future calls," Jones says. "To stop these annoying calls entirely, you can sign up for free services like Nomorobo, which automatically block unwanted robocalls while still allowing you to receive the ones that originate from trusted sources, like pharmacy refill reminders or Amber Alerts."

It takes extra effort, and a little help from Uncle Sam, your telecom provider and some good mobile apps, but you can go on the offensive against rude, unwanted telemarketers. Otherwise, those robocallers will keep pouring it on, day and night.

WASHINGTON -- The U.S. trade deficit widened in May, fueled by a drop in exports that could heighten concerns over weak overseas demand and a strong U.S. dollar.

The Commerce Department reported Tuesday that the trade gap grew $1.2 billion to $41.9 billion. That was less than the $42.6 billion deficit expected by analysts and suggests Wall Street economists may slightly raise their forecasts for economic growth in the second quarter.

But the drop in exports in May highlights a change in the tenor of economic growth since the United States exited the 2007-2009 recession. The economy relied more on export-led industries such as manufacturing early in the recovery, but growth is increasingly coming from domestic drivers like construction and services as the economic cycle matures.

Exports fell $1.5 billion, or 0.8 percent, to $188.6 billion in May, led by a drop in overseas sales of U.S.-made capital goods. Imports fell by about $300 million, or 0.1 percent, to $230.5 billion.

Prices for U.S. Treasuries rose after the data, while U.S. stock index futures were unchanged. The dollar gained against a basket of currencies.

Since the middle of last year when the Federal Reserve made clear it was planning to raise interest rates to keep the economy from eventually overheating, the dollar has strengthened, making U.S. exports less competitive.

Since that time, Europe's economy also has been on shaky ground and the European Central Bank has eased monetary policy, causing the euro to weaken against the dollar. European policymakers are currently fighting a debt crisis in Greece that threatens to rip apart the continent's monetary union.

Exports of goods to Germany fell 6 percent in May from the prior month, according to non-seasonally adjusted figures. Sales fell 4.2 percent to France, 2.1 percent to Mexico and 3 percent to Japan.

The U.S. economy contracted at a 0.2 percent annual rate in the first quarter, hit by bad weather, a strong dollar, spending cuts in the energy sector and disruptions at West Coast ports.

Other economic data, including figures on hiring and consumer spending, have pointed to a rebound during the second quarter, and a firming domestic economy could encourage the Fed to raise rates later this year.

In May, the drop in imports came as purchases from China rose 9.5 percent. That could fan further criticism from U.S. manufacturers that Chinese firms are using a cheap currency and unfair subsidies to gain market share in America.

At the same time, U.S. net imports of oil fell to $5.8 billion in May, the lowest level since 2002.

The Asahi Shimbun via Getty ImagesFormer Toyota executive Julie HampBy YURI KAGEYAMA

TOKYO -- The American Toyota executive who was arrested in Japan last month on suspicion of drug law violations is expected to be released Wednesday without being prosecuted, according to Japan's Kyodo News service.

Kyodo didn't identify the source of its information. Tokyo prosecutors declined to comment Tuesday. Toyota Motor (TM) said it had no information.

Julie Hamp, 55, who was the highest-ranking female executive at the Japanese automaker, was arrested June 18 on suspicion of bringing oxycodone, a narcotic pain killer, into Japan. The drug is tightly controlled here.

The drug was found by Japanese customs in a package that was sent to Hamp by mail from the U.S., police said.

Her appointment as head of communications in April had been highlighted by Toyota as a step toward promoting diversity.

Japan has among the poorest records in the industrialized world for gender equality in business and politics.

Hamp, who joined Toyota in 2012, worked in its U.S. operations until her latest promotion. Before that, she worked for PepsiCo (PEP) and General Motors (GM).

Hamp had been in the process of moving to Japan, the first foreign executive of Toyota to be permanently stationed in Japan. Toyoda has acknowledged the company should have done more to help her relocation.

She was arrested at a Tokyo hotel, where she had been staying while house-hunting.

Japanese media said the drugs were hidden in a package containing jewelry, and 57 pills were found. Police have refused to comment on such reports.

Police raided the automaker's headquarters in Toyota city, central Japan, as well as its Tokyo and Nagoya offices last month.

It is not unheard of for foreigners to be detained in Japan for mailing or bringing in medicine they used at home. Such drugs may be banned in Japan or require special approval. In Japan, suspects can be held in custody for up to 23 days without formal charges.

mindfrieze/Flickr

The United States Department of Defense is one of the biggest departments in the U.S. government. Fortunately, it's also one of the most transparent of government agencies, posting every contract it awards (aside from the penny-ante stuff -- there's a $6.5 million threshold for reporting) for public review on its website, and within mere hours of its being awarded.

Given the effort the Pentagon goes to in order to keep us informed of its spending, it would almost seem impolite not to take a look. And so that's what we just did over the holiday weekend. We tallied up all Pentagon contracts awarded in the month of June. And what did we find?

Aside from expenditures on servicemembers' salaries, health care and similar recurring "overhead," the Pentagon awarded $31.3 billion worth of contracts to defense contractors in the month of June.

Here are a few of the things they got for their (read: your) money...

20th-Century Technology

June was a month dominated by big-budget mega-contract awards. One of the biggest went to Boeing (BA), not coincidentally America's largest defense contractor by market cap. For $466.5 million, Boeing has been hired to repair guidance systems on U.S. Air Force Minuteman III intercontinental ballistic missiles. This contract will run through June 2, 2021.

22nd-Century Technology, Too

Smaller in size by far, but with potentially greater potential in years to come, were a quartet of contracts awarded early in the month to defense contractors Leidos Holdings (LDOS) and Ball Corp. (BLL). Leidos will receive $15 million on two contracts to conduct "laser interaction testing" and "target vulnerability assessments and data analysis" for the U.S. Air Force. Ball Corp will do similar but more extensive work, receiving a total of $32 million. Both companies will be researching the effects of high-power "continuous-wave (up to MW Class) and high energy pulsed (kJ) lasers interacting with individual materials, multi-material subsystems, and/or fully functional targets."

If successful, this work could accelerate the development of a whole new class of weapons for the U.S. military, potentially rendering the rest of the world's arsenal of explosives-based weapons obsolete.

Meanwhile, Back in the 21st Century ...

Somewhere between the realms of Cold War nukes and Buck Rogers laser weapons lie the more mundane parts of the Pentagon arsenal -- and these got plenty of funding as well. The U.S. military is preparing a wholesale makeover of its Air Force, replacing most of its planes with a new type of stealth fighter jet, the F-35 Lightning II. And in preparation for this, Lockheed Martin (LMT) was awarded $920 million last month to fund the purchase of "long lead time" parts needed to build 94 F-35 Lightning II stealth fighter jets for U.S. and foreign buyers. These will include:

o. 44 "standard" configuration F-35A fighters for the U.S. Air Force

o. 8 more for the Royal Australian Air Force

o. 6 for the Royal Norwegian Air Force

o. 2 each for the air forces of Italy and Turkey

o. and 16 more for unidentified "various foreign military sales customers"

o. 9 short take-off/vertical landing F-35B fighters for the U.S. Marine Corps

o. 3 F-35Bs for Britain

o. and 2 for Italy

o. and finally, 2 carrier-variant F-35Cs for the United States Navy.

And an Aircraft Carrier to Carry Them

Speaking of those carrier variants, they're going to need ships to fly from -- and Huntington Ingalls (HII) has that covered. On June 5, the Pentagon awarded the company two separate contracts, worth a total of $4.3 billion combined, to complete design and construction work on the new nuclear aircraft carrier USS John F. Kennedy by June 2022. Once entered into service, the Kennedy will be the second of the new Gerald R. Ford-class supercarriers, of which four are expected to be built.

$4.3 Billion?! I Need an Aspirin...

If the volumes of dollars being thrown around at the Pentagon are giving you a headache, McKesson (MCK) has got you covered -- with an even bigger contract. In fact, weighing in at $6.1 billion, this company's 30-month award to supply "replenishment pharmaceuticals to furnish the Tricare pharmacy supporting 9.5 million active-duty service members, retirees and their dependents" was the single largest contract awarded by the Pentagon in the month of June.

A renewal of a smaller, $2.6 billion award granted to McKesson back in December 2012, this contract may be renewed as many as two more times over the coming seven and a half years. Ultimately, it could last as long as a decade, and be worth as much as $12.3 billion to McKesson.These contracts represent only a small sampling of the hundreds of awards your tax dollars funded last month. To see the rest, check out the U.S. Department of Defense contracts website here.

Think $4.3 billion is a lot to spend on an aircraft carrier? Motley Fool contributor Rich Smith recently read that Americans spend about $1 billion a year on fireworks for July Fourth, New Year's, and other holidays. And those don't even blow stuff up. (At least, not intentionally.) Follow him on Facebook for more defense news.

Rich owns none of the stocks mentioned above, but The Motley Fool recommends McKesson. Try any of our Foolish newsletter services free for 30 days and check out our free report on one great stock to buy for 2015 and beyond.